How is unrecaptured 1250 gain treated?

How can I reduce unrecaptured Section 1250 gains? Unrecaptured Section 1250 gains can be offset by capital losses. For a capital loss to offset a capital gain, they both must be either a short-term capital gain or a long-term capital gain.

How does Section 1250 recapture work?

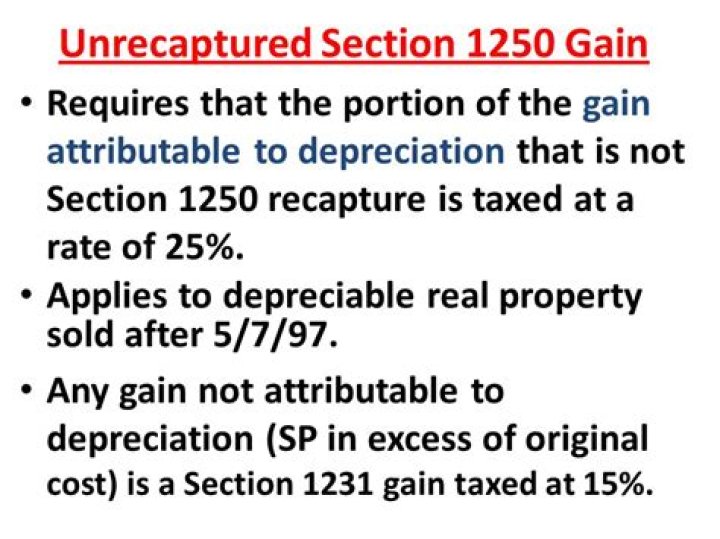

An unrecaptured section 1250 gain is an income tax provision designed to recapture the portion of a gain related to previously used depreciation allowances. It is only applicable to the sale of depreciable real estate. Unrecaptured section 1250 gains are usually taxed at a 25% maximum rate.

How does recapture work on SEC 1250 real estate?

Gain from selling Sec 1250 property (real estate) is subject to recapture – the excess of the actual amount of depreciation previously claimed for the property over the amount of depreciation that would have been allowable under the straight-line method, limited to the gain on the sale, is taxed as ordinary income.

How are unrecaptured Section 1250 gains offset?

Unrecaptured section 1250 gains can be offset by capital losses. A section 1250 gain is recaptured upon the sale of depreciated real estate, just as with any other asset; the only difference is the rate at which it is taxed.

What does it mean to have a Section 1250 property?

(c)Section 1250 property. For purposes of this section, the term “section 1250 property” means any real property (other than section 1245 property, as defined in section 1245(a)(3)) which is or has been property of a character subject to the allowance for depreciation provided in section 167.

How are recapture and Unrecaptured real estate gains taxed?

Recaptured and Unrecaptured Real Estate Rental Section 1250 Gain. But the amount of depreciation claimed on Sec 1250 property that is not recaptured as ordinary income under the Sec1250 recapture rules is unrecaptured section 1250 gain, and is subject to a special capital gain tax rate of 25%.