How long can a net operating loss be carried forward?

At the federal level, businesses can carry forward their net operating losses indefinitely, but the deductions are limited to 80 percent of taxable income. Prior to the Tax Cuts and Jobs Act (TCJA) of 2017, businesses could carry losses forward for 20 years (without a deductibility limit).

Where is net operating loss carryover?

The full amount of NOL carryover available will show per IRS guidelines: Publication 536: If you carry forward your NOL to a tax year after the NOL year, list your NOL deduction as a negative figure on the “Other income” line of Schedule 1 (Form 1040) or Form 1040NR (line 8 for 2020).

What is carry back of losses?

What Is a Loss Carryback? A loss carryback describes a situation in which a business experiences a net operating loss (NOL) and chooses to apply that loss to a prior year’s tax return. This results in an immediate refund of taxes previously paid by reducing the tax liability for that previous year.

When to use net operating loss carryback and carryforward?

The net operating loss carryback and carryforward. When a business reports operating expenses on its tax return that exceed its revenues, a net operating loss (NOL) has been created. An NOL can be used in some other tax reporting period as an offset to taxable income, which reduces the tax liability of the reporting entity.

What is the difference between Nol carryback and carryforward?

Tax Loss Carryback and Carryforward. Tax loss carryback is when a corporation retrospectively adjusts its tax returns for prior periods if it incurs a net operating loss (NOL) in current period. Tax carryforward is when a corporation subtracts net operating loss from future period income.

When to use a net operating loss ( NOL )?

When a business reports operating expenses on its tax return that exceed its revenues, a net operating loss (NOL) has been created. An NOL can be used in some other tax reporting period as an offset to taxable income, which reduces the tax liability of the reporting entity. The basic rules for using an NOL are:

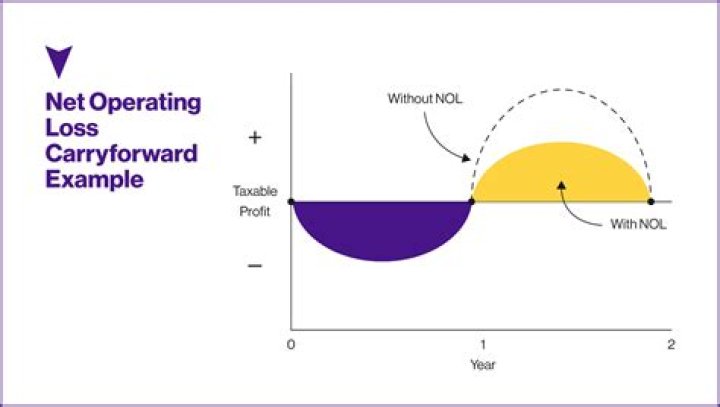

What is an example of tax loss carryforward?

Tax loss carryforward results in recognition of a deferred tax asset. Let’s continue with our example above. $25 million of net operating loss related to 2017 couldn’t be carried back because the corporation ran out of available taxable income. The remainder of the NOL which can’t be carried back can be carried back for 20 years.