How long can you do an interest-only loan?

Interest-only periods usually last between three and five years. Some lenders offer interest-only periods of up to 10 to 15 years, but this may be restricted to investors. You may be able to negotiate the length of the interest-only period with your lender, depending on your personal circumstances.

How do I qualify for an interest-only loan?

Who’s eligible for an interest-only home loan? Interest-only loans require a higher credit score, income and down payment. There may also be additional requirements around assets, cash reserves (having six to 12 months’ of mortgage payments in the bank) and a lower debt-to-income ratio.

Can you pay only the interest on a loan?

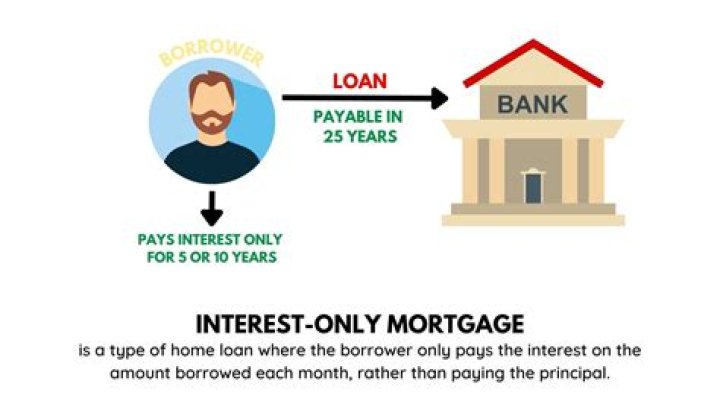

Those with an interest-only mortgage only pay the interest on the loan for a set period of time, typically the first 5 – 10 years of the loan. Fixed-rate interest-only options are rare. Usually, interest-only mortgages come baked into some type of adjustable rate structure. (More on this later.)

Why would you get an interest-only loan?

Advantages of Interest-Only Loans That allows borrowers to afford a more expensive home. That only works if the borrower plans to make the higher payments after the introductory period. For example, some increase their income before the intro period is over. Others plan to sell the home before the loan converts.

What is the maximum interest-only period?

To help manage risks, lenders also typically limit the maximum interest-only period to five years. The role of interest-only lending and its potential implications for financial stability have been of interest to the Reserve Bank for some time.

What is a interest only loan example?

The option to pay interest only lasts for a specified period, usually 5 to 10 years. Borrowers have the right to pay more than interest if they want to. For example, if a 30-year loan of $100,000 at 6.25% is interest only, the required payment is $520.83.