How long do I amortize start up costs?

If your startup expenditures actually result in an up-and-running business, you can: Deduct a portion of the costs in the first year; and. Amortize the remaining costs (that is, deduct them in equal installments) over a period of 180 months, beginning with the month in which your business opens.

What is the entry of amortization?

To record annual amortization expense, you debit the amortization expense account and credit the intangible asset for the amount of the expense. A debit is one side of an accounting record. A debit increases assets and expense balances while decreasing revenue, net worth and liabilities accounts.

How many years can you amortize?

15 years

IRS Amortization Rules Unless otherwise stated in IRS regulations, you must amortize your intangible assets over a maximum period of 15 years. You must use the straight-line method to calculate the amortization deduction. Intangible assets are amortized at their full value since there is no salvage value to deduct.

What do you mean by amortization?

Amortization is an accounting technique used to periodically lower the book value of a loan or an intangible asset over a set period of time. In relation to a loan, amortization focuses on spreading out loan payments over time. When applied to an asset, amortization is similar to depreciation.

Does amortization reduce taxes?

You can deduct amortization expenses to reduce your tax liability. Deducting amortization lowers taxable earnings and shrinks your year-end tax bill. You can deduct a portion of the cost of an intangible asset for each year that it’s in service until it has no further value.

How long do you amortize customer list?

Customer list #2 is an amortizable Sec. 197 intangible, subject to 15-year amortization, because it is a customer list obtained as part of acquiring a business.

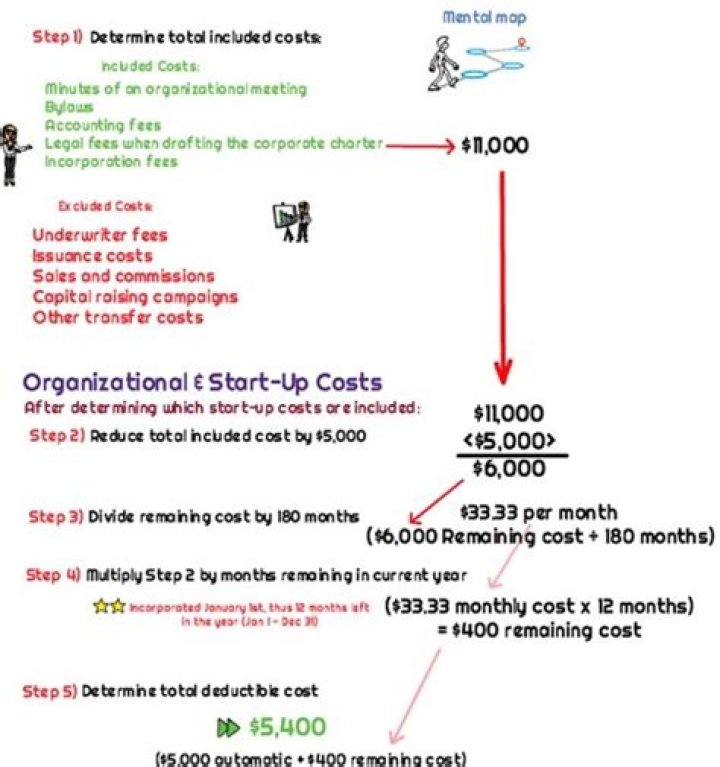

How long does it take for start up costs to be amortized?

Start-up costs are typically capitalized or amortized over 15 years. However, up to $5,000 of these expenses are eligible to be expensed as a deduction. The remainder is amortized over 15 years.

When does amortization expense occur in an accounting period?

When an asset is purchased (or disposed of) at a time other than the beginning or end of an accounting period, amortization expense is calculated for a part of that year. This is essential because due to the matching principle, we have to record an expense for the portion of the year that the capital asset generated revenues.

When does amortization of intangible assets start?

1. The amortization of an asset should only start when the asset is brought into actual use, and not before, even if the requisite intangible asset has been acquired. 2. The level amortization should be appropriate so that the book value of an asset is not under or overstated.

How to calculate the amortization of a patent?

If you assumed the patent was useful for 20 years, but after 10 years the value of the technology became useless, you can expense (write off) the remaining value. Calculate the amortization per year. Use this formula: Initial cost / useful life = amortization per year. Therefore, $50,000 / 20 = $2,500.