How much of your gross income can you afford?

To calculate ‘how much house can I afford,’ a good rule of thumb is using the 28%/36% rule, which states that you shouldn’t spend more than 28% of your gross monthly income on home-related costs and 36% on total debts, including your mortgage, credit cards and other loans like auto and student loans.

How much home can I afford based on gross income?

Why it’s smart to follow the 28/36% rule Most financial advisers agree that people should spend no more than 28 percent of their gross monthly income on housing expenses and no more than 36 percent on total debt — that includes housing as well as things like student loans, car expenses and credit card payments.

Why is affordability based on gross income?

If you’re looking to apply for a mortgage, your gross income is key to knowing how much you can afford. Mortgage lenders and landlords use your gross income to determine your financial reliability. Lenders want to know what percentage of your income will go to a mortgage payment.

How much house can you afford if you make $40000 a year gross income?

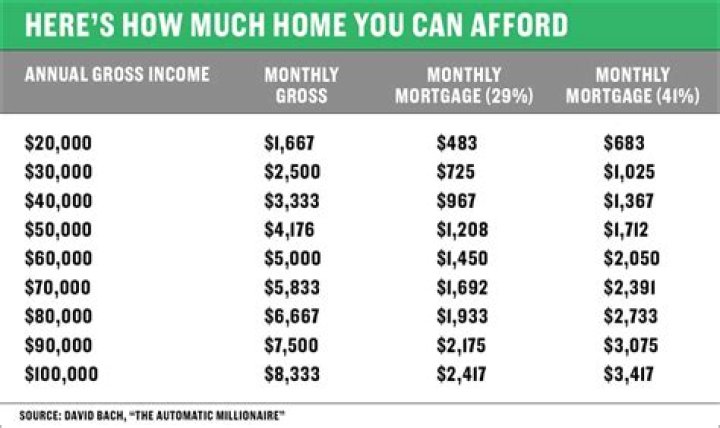

Example. Take a homebuyer who makes $40,000 a year. The maximum amount for monthly mortgage-related payments at 28% of gross income is $933. ($40,000 times 0.28 equals $11,200, and $11,200 divided by 12 months equals $933.33.)

What do you use your gross income for?

Your gross income is also used when you apply for other types of loans including credit cards as wells as car and personal loans.

How does the mortgage company use your gross income?

Lenders use your monthly gross income to determine how much you can spend on your mortgage payment and total monthly housing expense, which included property tax, homeowners insurance and other applicable fees such as homeowners association dues.

What should your mortgage payment be as a percentage of your income?

One week’s paycheck is about 23 percent of your monthly (after-tax) income. If I had to set a rule, it would be this: Aim to keep your mortgage payment at or below 28 percent of your pretax monthly income. Aim to keep your total debt payments at or below 40 percent of your pretax monthly income.

Can a person with higher gross income qualify for a larger mortgage?

Borrowers with higher monthly gross income and lower debt payments can afford to spend more on their mortgage payment which enables them to qualify for a larger mortgage. Borrowers who want to increase the mortgage amount they qualify for should pay down their debt to boost their debt-to-income ratio before they apply for a mortgage.