How often do mortgage companies do escrow analysis?

Yearly Escrow Analysis To ensure that the cushion in your escrow account isn’t ever too large, RESPA requires lenders to perform an analysis of your escrow account at least once each year. During this analysis, the lender projects the balance of the account for 12 months into the future.

Does escrow reset every year?

Going Forward. The lender repeats this process every year. It can be difficult to anticipate if your costs will go up or down. To avoid unpleasant surprises, pay attention to correspondence from your insurance company or taxing authority.

How often must a lender perform an escrow account analysis?

For each escrow account, the servicer must conduct an escrow account analysis at the completion of the escrow account computation year to determine the borrower’s monthly escrow account payments for the next computation year, subject to the limitations of paragraph (c)(1)(ii) of this section.

Can you request an escrow analysis at any time?

If you don’t agree with the analysis – if you think your lender is collecting too much or too little for escrow – you can request a re-evaluation at any point following receipt of the initial escrow analysis.

What should your escrow balance be?

It’s typically twice your monthly escrow contribution — per the federal Real Estate Settlement Procedures Act (RESPA). For example, if you’re required to put $500 a month into escrow, your minimum required balance would typically be $1,000. The CFPB notes that this gives you a two-month cushion.

Why do I have an escrow shortage every year?

The most common reason for a shortage – or an increase in your payments – is an increase in your property taxes. In other words, an escrow shortage is the result of not having enough money in your escrow account to cover the actual amount needed to pay your bills.

What happens to your escrow account when you get a mortgage?

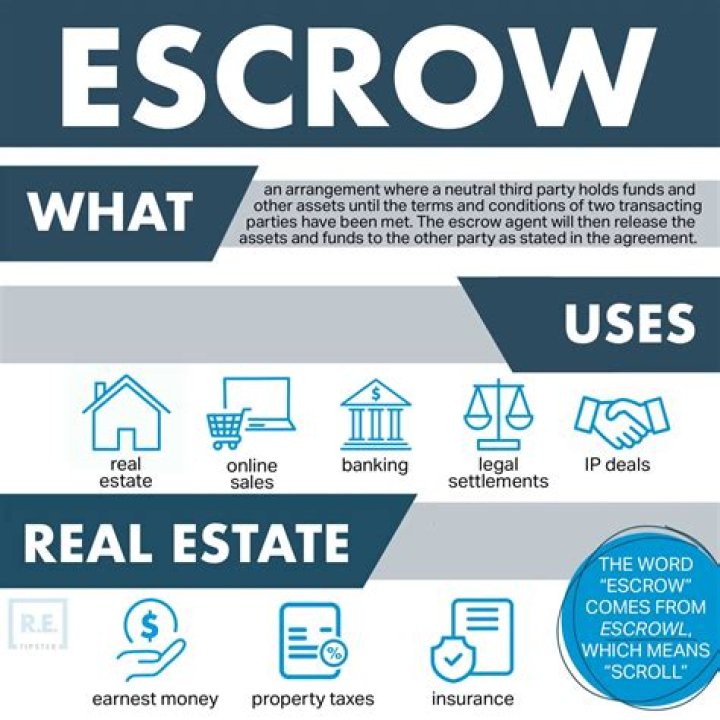

When you get a mortgage loan, the lender is going to add real estate taxes and insurance premiums to the monthly payment. The lender is going to set this money aside into a separate account, and that’s your escrow account.

Where do I find the escrow details on my mortgage?

Sign on to your mortgage account online and select the Escrow Details link to see the most recent amounts paid for your property taxes and insurance premiums. Keep in mind that these amounts reflect payments we’ve already made. If they don’t match your most recent tax and insurance bills, it’s because we haven’t paid those yet.

Who are the middlemen in a mortgage escrow account?

In layman’s terms, this means an escrow service is basically a middleman between a buyer and a seller, or in the case of a mortgage, a middleman between a homeowner and the county (for property taxes), insurance companies, and anyone else who the homeowner designates to pay with funds from the escrow account.

How often do payments need to be held in escrow?

To ensure there’s enough cash in escrow, most lenders require around 2 months’ worth of extra payments to be held in your account. Your lender or servicer will analyze your escrow account annually to make sure they’re not collecting too much or too little.