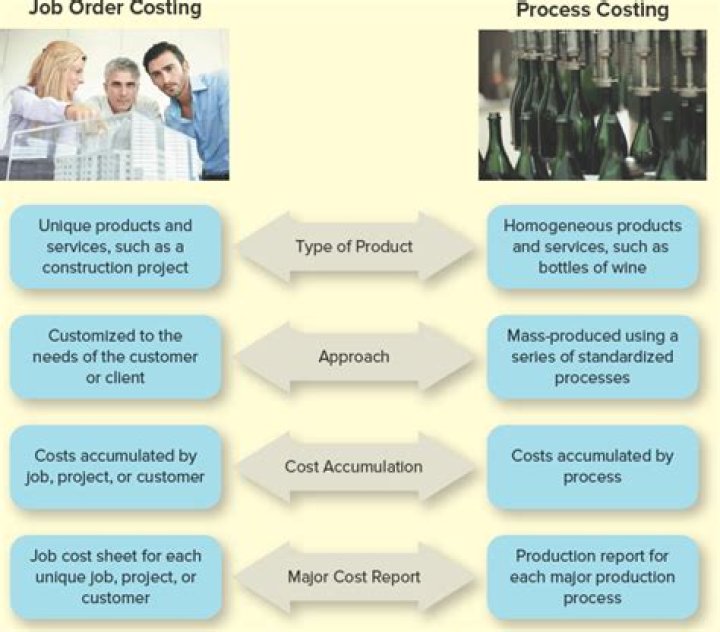

In what ways are job order costing and process costing similar?

Job costing and process costing have important similarities: Both job and process cost systems have the same goal: to determine the cost of products. Both job and process cost systems have the same cost flows. Accountants record production in separate accounts for materials inventory, labor, and overhead.

Why are equivalent units of production used in process costing?

An equivalent unit of production is an expression of the amount of work done by a manufacturer on units of output that are partially completed at the end of an accounting period. Equivalent units are used in the production cost reports for the producing departments of manufacturers using a process costing system.

Which cost accounting system is much better job order costing or process costing?

Job costing is used for very small production runs, and process costing is used for large production runs. Record keeping. Much more record keeping is required for job costing, since time and materials must be charged to specific jobs. Process costing aggregates costs, and so requires less record keeping.

What are equivalent units of production in process costing?

In cost accounting, equivalent units are the units in production multiplied by the percentage of those units that are complete (100 percent) or those that are in process. That covers everything. If a unit is completed and transferred out, it’s 100 percent complete.

What is job order costing explain with example?

Job order costing is a costing method which is used to determine the cost of manufacturing each product. This costing method is usually adopted when the manufacturer produces a variety of products which are different from one another and needs to calculate the cost for doing an individual job.

How do you calculate equivalent units of production?

Equivalent units. are calculated by multiplying the number of physical (or actual) units on hand by the percentage of completion of the units. If the physical units are 100 percent complete, equivalent units will be the same as the physical units.

How do you calculate equivalent production?

Here’s the formula:

- The number of partially completed units x percentage of completion = equivalent units of production.

- 300 x .5 = equivalent units of production.

- equivalent units of production = 150.

- 500 + 150 = 650 equivalent units of production.

- Total equivalent units for a cost component = A + B × C.

- Where.

What do you mean by equivalent units of production?

Equivalent units of production is a term applied to the work-in-process inventory at the end of an accounting period. In short, if 100 units are in process but you have only expended 40% of the processing costs on them, then you are considered to have 40 equivalent units of production.

What is the formula for unit cost?

Unit cost is determined by combining the variable costs and fixed costs and dividing by the total number of units produced. For example, assume total fixed costs are $40,000, variable costs are $20,000, and you produced 30,000 units.

How do you prepare a production cost report?

(Steps Enumerated in the Production Report) 1: Analyze the physical flow of production units. 2: Calculate equivalent units for each manufacturing cost element. 3: Determine total costs for each manufacturing cost element. 4: Compute cost per equivalent unit for each manufacturing cost element.

Does Apple use job order costing?

The main benefits include improving business process and identifying wasteful products in the production process. Apple Inc. uses the activity-based costing method to value its products. (Job costing or job order costing is a system used to collect and assign manufacturing costs to units that vary from one another.)