Is a capital lease an operating asset?

The capital lease requires a renter to book assets and liabilities associated with the lease if the rental contract meets specific requirements. In essence, a capital lease is considered a purchase of an asset, while an operating lease is handled as a true lease under generally accepted accounting principles (GAAP).

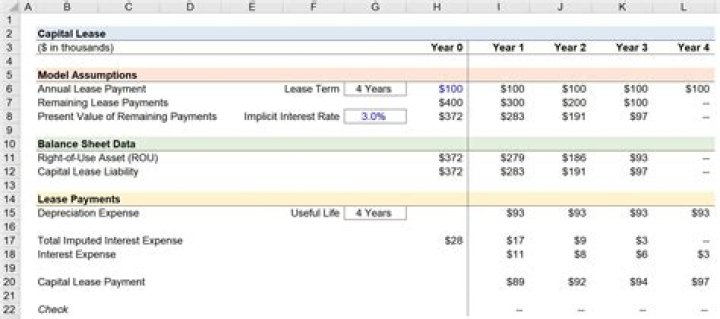

How does a capital lease work?

Description: In a capital lease, the lessor transfers the ownership rights of the asset to the lessee at the end of the lease term. The lease agreement gives the lessee a bargain option by dint of which the lessee can buy the asset at a discounted price than the fair market value at the end of the lease term.

Are operating leases capitalized now?

Capitalizing Operating Leases The new rule, FASB ASU (Accounting Standards Update) 2016.02, will require that all leases with a term over one year must be capitalized effective for years beginning after 12/15/2021. Operating leases will need to be recorded as equal and offsetting amounts of assets and liabilities.

Why is operating lease better than capital lease?

Operating leases provide greater flexibility to companies as they can replace/update their equipment more often. No risk of obsolescence, as there is no transfer of ownership. Accounting for an operating lease is simpler. Lease payments are tax-deductible.

Is operating lease cancellable?

So what is included in the “operating leasing” industry is such asset renting where the user needs the asset for long term, but he does not commit himself to any permanent usage or a very long term. In other words, the lease is long term, but is cancellable.

What’s the difference between an operating lease and a capital lease?

A capital lease (or finance lease) is treated like an asset on a company’s balance sheet, while an operating lease is an expense that remains off balance sheet. Think of a capital lease like owning a property and think of an operating lease like renting a property.

How are operating leases classified on a balance sheet?

Historically, operating leases have enabled American firms to keep billions of dollars of assets and liabilities from being recorded on their balance sheets. To be classified as an operating lease, the lease must meet certain requirements under generally accepted accounting principles (GAAP) that exempt it from being recorded as a capital lease.

Who are the accounting agencies for capital leases?

Several accounting and financial reporting agencies and boards regulate how businesses report their finances, including accounting for capital and operating leases. The two main agencies are the Financial Accounting Standards Board (FASB) in the U.S. and the International Accounting Standards Board (IASB) internationally.

What are the requirements for a capital lease?

To be classified as a capital lease under U.S. GAAP, any one of four conditions must be met: A transfer of ownership of the asset at the end of the term. An option to purchase the asset at a discounted price at the end of the term. The term of the lease is greater than or equal to 75% of the useful life of the asset.