Is a charitable trust revocable or irrevocable?

Charitable trusts are irrevocable. After all, it would be awkward for the law to allow giving to a charity and then taking it back! You can arrange for the charity to receive income for a certain number of years, and later the remaining income.

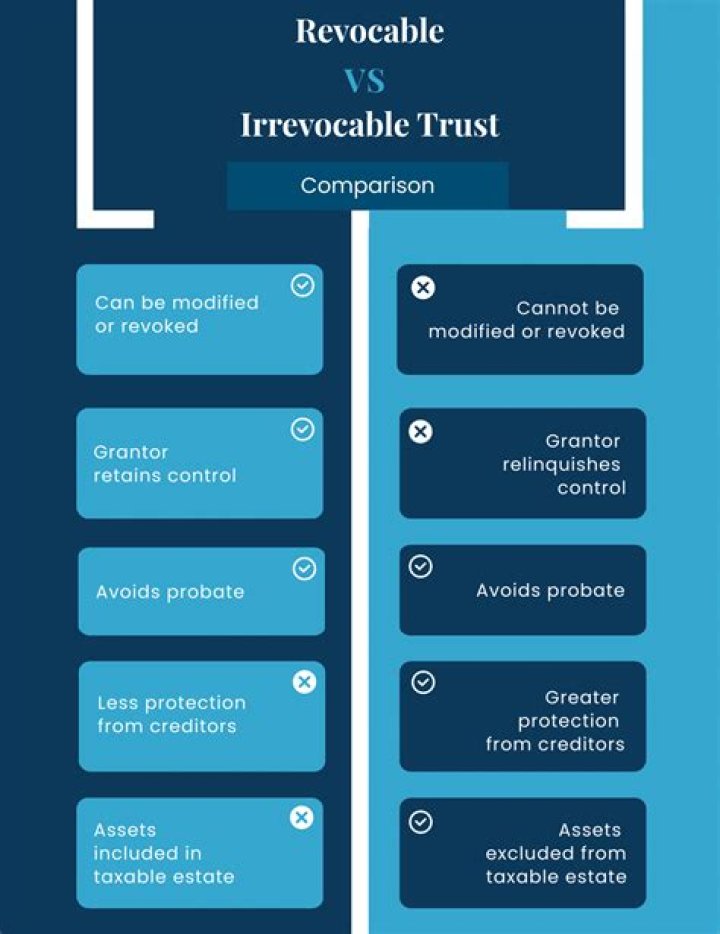

What is irrevocable and revocable?

A revocable trust and living trust are separate terms that describe the same thing: a trust in which the terms can be changed at any time. An irrevocable trust describes a trust that cannot be modified after it is created without the consent of the beneficiaries.

Why does a revocable trust become irrevocable upon death?

Why Does a Revocable Trust Turn Irrevocable Once the Grantor Dies? On the other hand, Irrevocable trusts are those that cannot be changed even by the grantor once they are formed and funded. Every revocable trust becomes irrevocable when the creators of the trust died.

When does a revocable trust become an irrevocable trust?

A revocable living trust becomes irrevocable when the grantor dies because he’s no longer available to make changes to it. But a revocable trust can be designed to break into separate irrevocable trusts at the time of the grantor’s death for the benefit of children or other beneficiaries.

Can a grantor name a trustee for a revocable trust?

The grantor can name the trustee, someone they trust to take over in the event that they can no longer personally manage the trust themselves. Revocable trusts also avoid probate of the assets they hold.

Can a grantor claim a tax deduction on an irrevocable trust?

The grantor can claim a charitable income tax deduction in the year the transfer is made to the irrevocable trust if the initial funding of assets into the trust is made while they’re still alive.

How does an irrevocable life insurance trust work?

Irrevocable life insurance trusts are set up to accept life insurance benefits at the time of the grantor’s death. This can take a sizable chunk of value out of an estate that’s potentially subject to the estate tax, bringing the value down below that year’s estate tax exemption threshold.