Is a promissory note required?

Loan Amounts, Fees & Interest Rates All promissory notes are required to provide the original amount of the loan and the interest rate. For instance, if you agree to a fixed rate but default on your loan, the lender can change the interest rate if you agreed to this term in the original note.

Who can issue promissory note?

Promissory notes are debt instruments. They can be issued by financial institutions. The capital markets consist of two types of markets: primary and secondary.

Why do you need a promissory note?

A promissory note evidences an obligation to repay a loan. In transactions using a loan or credit agreement, promissory notes typically reference the loan agreement, requiring a reading of both documents to fully understand the terms.

How are promissory notes calculated?

For example, for a nine-month promissory note, divide 9 by 12 (the number of months in a year) to equal 0.75. Multiply 750 by 0.75 to equal 562.50. Likewise, for a daily time period, multiply the product by the ratio of days to years.

How is a promissory note used in a loan?

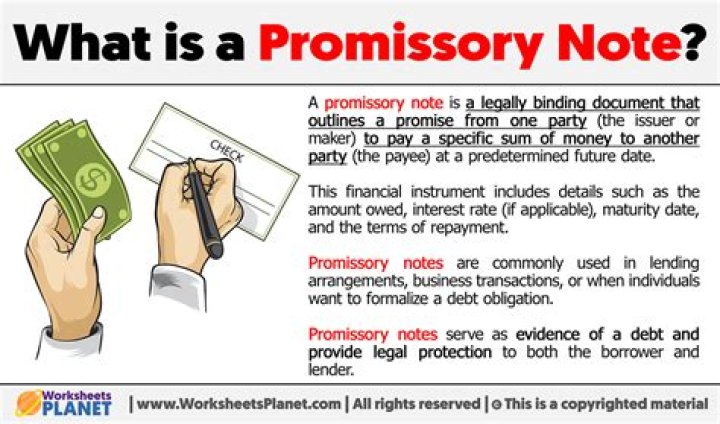

Use our Promissory Note to detail the terms of loan repayment. A promissory note is a written and enforceable agreement in which a borrower promises to pay a lender a sum of money on demand, or within a specified period of time.

Who is on the hook for a promissory note?

1. Who is on the hook? (the “borrower” and the “lender”) A standard promissory note should name who is receiving money or a line of credit (the “borrower”) and who will be repaid (the “lender”). Only the borrower must sign the promissory note, but it is good practice to also include the lender’s signature. 1.

Can a promissory note be written on a napkin?

A promissory note written on a napkin could be valid if the required terms are included. Alternative names for promissory notes include: IOU, personal notes, loan agreements, notes payable, note, promissory note form, promise to pay, secured or unsecured notes, demand notes, or commercial paper.

What happens if you refuse to pay a promissory note?

If the borrower refuses to pay, the promissory note provides strong evidence if the lender wishes to initiate legal action. In the event that the borrower loses the lawsuit, they would also be responsible for paying any reasonable costs associated with the collection of debts, including attorney fees.