Is a shareholder loan income?

Shareholders may take a loan from the corporation and are not required to report it as personal income on their personal tax return for that fiscal tax year. A loan to a shareholder must be returned to the corporation by the end of the next fiscal year to ensure that the amount will not be taxed.

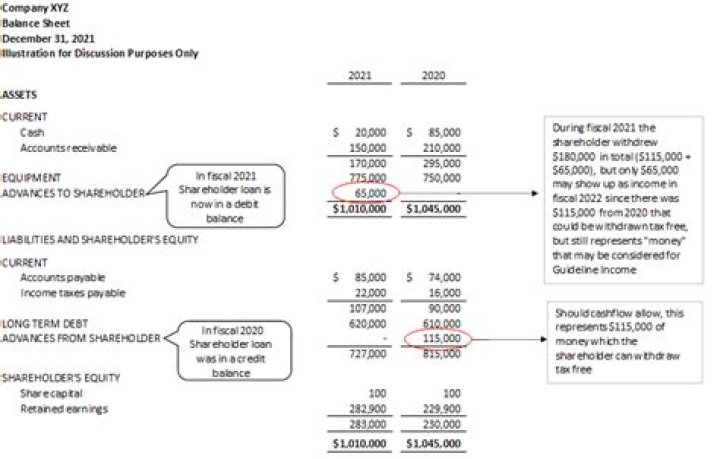

How do you classify a shareholder loan?

Shareholder loan is a debt-like form of financing provided by shareholders. Usually, it is the most junior debt in the company’s debt portfolio. On the other hand, if this loan belongs to shareholders it could be treated as equity. Maturity of shareholder loans is long with low or deferred interest payments.

How do you withdraw money from a corporation?

You can withdraw funds from your corporation by having your corporation declare a dividend. Once a dividend is declared on a particular class of shares, all shareholders with that class of shares must receive such a portion of the declared dividend in proportion to the number of the shares held.

Can a shareholder loan money to a company?

Shareholders often loan money to their corporation in order to keep the business operating. There are rules and regulations in the Internal Revenue Code (IRC) that must be adhered to in order for loans to be treated as such, and not an equity contribution.

When to repay loan from shareholders’s Corp?

On January 4, the first business day of the second year of operation, Jones’ Corporation receives its loan from a bank and repays the loan given by the shareholder. This shareholder’s loan basis would increase to the extent of the loan balance at the end of year two for the income that passed through the business.

What’s the difference between a shareholder loan and employee loan?

The Tax Guy refers to this as the principle residence rule. Do not confuse these loans to shareholder with shareholder loans where you made to the corporation as an investment in the business. These rules only apply when the corporation lends the shareholder/employee money.

When is a loan made to a shareholder taxable?

Generally, when a loan is made by the corporation to a shareholder, a taxable benefit arises for the shareholder. The amount received must be included in the recipient’s income in the year the money was received. When the loan is repaid, it can be deducted from income in the year of payment. However, there are exceptions to this rule.