Is accrued interest a personal account?

Accrued interest is a representative personal account indirectly linked to the person, and is shown on the assets side of a balance sheet.

How do you record accrued interest paid?

When you take out a loan or line of credit, you owe interest. You must record the expense and owed interest in your books. To record the accrued interest over an accounting period, debit your Interest Expense account and credit your Accrued Interest Payable account. This increases your expense and payable accounts.

What does it mean to have accrued interest?

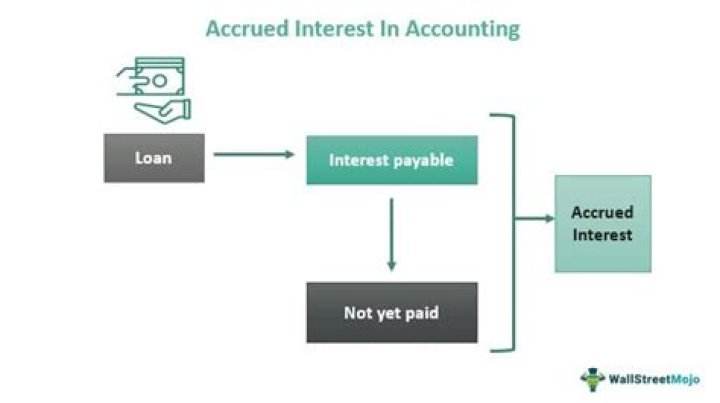

Accrued interest is an accounting term that refers to the amount of interest that has been incurred as of a specific date but has not yet been paid. Accrued interest can be two-sided, i.e., it can be in the form of accrued interest expense owed by the borrower or accrued interest income on customer deposits that are owed by the bank.

What kind of accounts are used to record accrued interest?

How you create an accrued interest journal entry depends on whether you’re the borrower or lender. If you’re the borrower, you’ll work the following accounts: Interest Expense account; Accrued Interest Payable account; If you’re the lender (e.g., extending credit), you’ll work with these accounts: Accrued Interest Receivable account

How does accrued interest relate to the matching principle?

The application of accrued interest is a result of accrual accounting which counts economic events when they occur regardless of receipt of payment. It is the method associated with the matching principle of accounting.

When to use 30 day or 360 day accrued interest?

The other one is the 30/360 convention, assuming 30 days for a month and 360 days for a year, which is usually used for corporate bonds. The amount of accrued interest should be earned by the bond seller. The quoted price in the bond market, known as the clean price or flat price, does not include any accrued interest.