Is business equipment taxable?

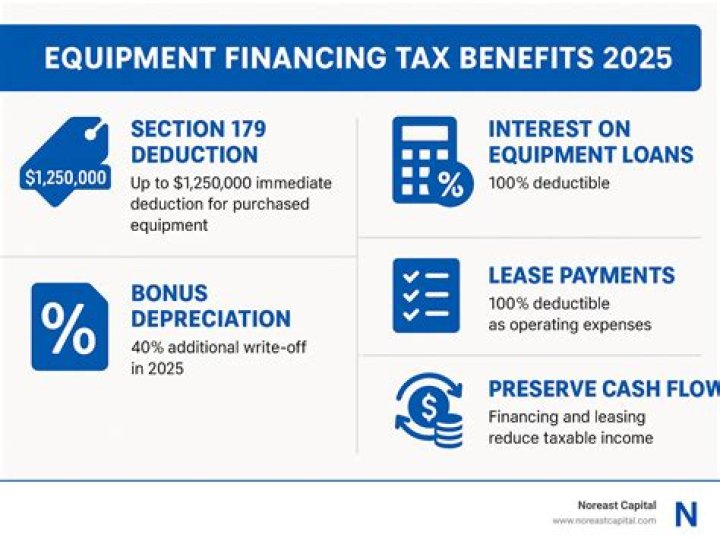

The IRS allows business owners to expense the entire depreciable basis of equipment in the year of the purchase. Businesses must have taxable income before using section 179; they cannot reduce taxable income below zero and are limited to an IRS determined maximum, which is currently $1,000,000.

Are equipment payments tax deductible?

You can deduct the entire cost of the equipment if you financed it. You can also deduct the interest you paid. This is referred to as a first-year expense or Section 179 deduction.

Where does equipment go on a business tax return?

This is usually deducted as “small tools and equipment” expense on a business tax return. Many pieces of equipment with a lifespan that is over one year are classified as capital assets.

Can you depreciate business equipment for tax purposes?

These two types of purchases are considered in different ways for accounting and tax purposes. Some purchases, especially those of a smaller amount, can be expensed, while other purchases, usually equipment, must be depreciated. First, note that these purchases are for business purposes only, not for personal use.

How is the purchase of business equipment accounted for?

The purchase of equipment is not accounted for as an expense in one year; rather the expense is spread out over the life of the equipment. This is called depreciation. From an accounting standpoint, equipment is considered capital assets or fixed assets, which are used by the business to make a profit. Taxes on Sales of Business Equipment

Can a machinery purchase be exempt from tax?

Sellers must obtain a written certificate from the purchaser that certifies the purchaser’s entitlement to the exemption. If so, the seller is relieved of liability and the Department should look solely to the buyer. Also exempt from tax is industrial machinery and equipment purchased for use in aquacultural activities at a fixed location.