Is cash collection an operating activity?

Examples of the direct method of cash flows from operating activities include: Cash collected from customers. Interest income and dividends received.

What is a cash inflow?

Cash inflow is the money going into a business. That could be from sales, investments or financing. It’s the opposite of cash outflow, which is the money leaving the business. A business is considered healthy if its cash inflow is greater than its cash outflow.

What are cash collection items?

Cash collection, also known as payment collection, is a treasury function that describes the process whereby a company recovers cash from other businesses (or individuals) to whom it has previously issued an invoice. The key objective of cash collection is to get invoices paid on their due date.

What makes up cash flow from operating activities?

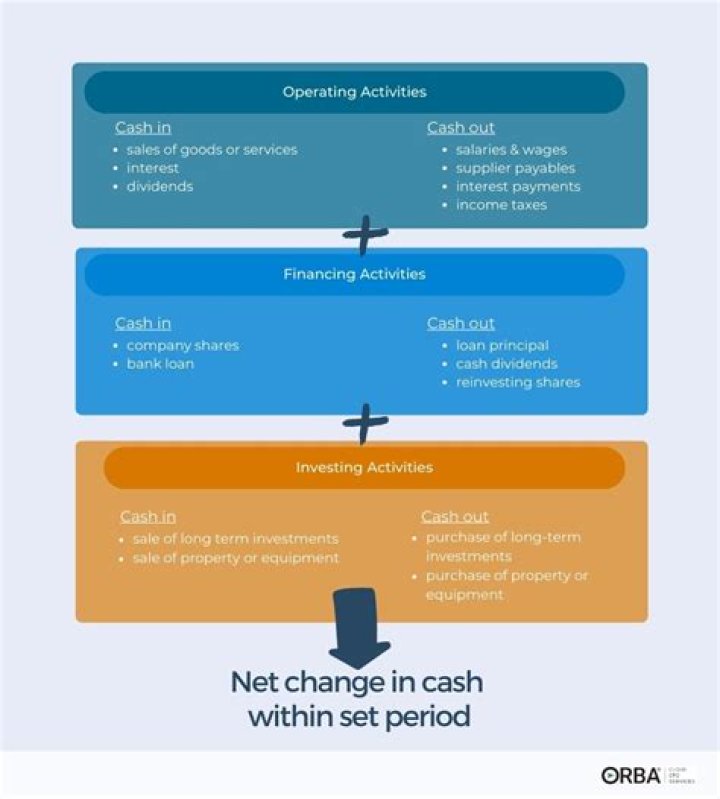

What is Cash Flow from Operations? Cash flow from operations is the section of a company’s cash flow statement that represents the amount of cash a company generates (or consumes) from carrying out its operating activities over a period of time. Operating activities include generating revenue

Which is the first section of the cash flow statement?

It is the first section depicted on a company’s cash flow statement. Cash flow from operating activities does not include long-term capital expenditures or investment revenue and expense. CFO focuses only on the core business, and is also known as operating cash flow (OCF) or net cash from operating activities.

How to reconcile net income to cash flows from operations?

The indirect method uses changes in balance sheet accounts to reconcile net income to cash flows from operations. Assets = Liabilities + Stockholders Equity Cash + Noncash Assets = Liabilities + SE Cash = L + SE – NCA ∆ Cash = ∆ L + ∆ SE – ∆ NCA This means that we can evaluate changes in cash by looking at changes in balance sheet accounts.

Which is the best definition of investing cash flows?

investing cash flows) are the cash inflows and outflows that relate to acquiring and disposing of operating assets and investments in other companies (current and long-term), lending money, and collecting loans Cash flows from investing activities Cash Inflows/Outflows