Is Conceptual Framework a standard?

Conceptual Framework a framework for setting accounting standards; a basis for resolving accounting disputes; fundamental principles which then do not have to be repeated in accounting standards.

Can Conceptual Framework override financial reporting standards?

Status and Purpose of the Conceptual Framework Nothing in the Conceptual Framework overrides any Standard or any requirement in a Standard. SP1. 3 To meet the objective of general purpose financial reporting, the MASB may sometimes specify requirements that depart from aspects of the Conceptual Framework.

Does the Conceptual Framework override any specific standards?

Status and purpose of the Conceptual Framework. It maintains that the framework does not override any specific IFRS.

What is Conceptual Framework for financial reporting?

The Conceptual Framework (or “Concepts Statements”) is a body of interrelated objectives and fundamentals. The objectives identify the goals and purposes of financial reporting and the fundamentals are the underlying concepts that help achieve those objectives.

How do you explain conceptual framework?

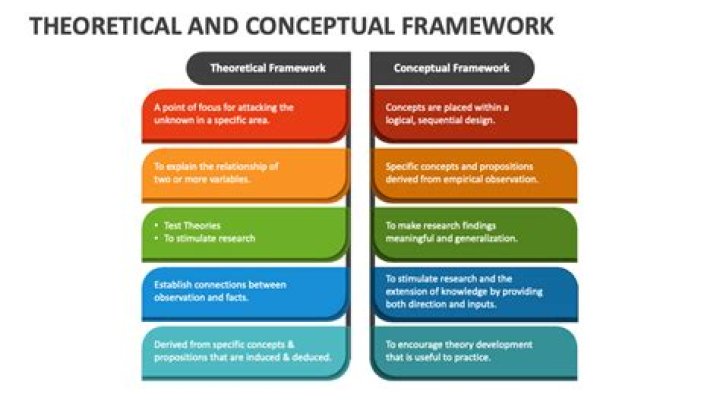

A conceptual framework is a written or visual representation of an expected relationship between variables. Variables are simply the characteristics or properties that you want to study. The conceptual framework is generally developed based on a literature review of existing studies and theories about the topic.

What are the basic purposes of the conceptual framework?

The primary purpose of the Conceptual Framework was to assist the IASB in the development of future IFRSs and in its review of existing IFRSs. The Conceptual Framework may also assist preparers of financial statements in developing accounting policies for transactions or events not covered by existing standards.

What are the components of the conceptual framework for financial reporting?

The Framework addresses:

- the objective of general purpose financial reporting.

- qualitative characteristics of useful financial information.

- financial statements and the reporting entity.

- the elements of financial statements.

- recognition and derecognition.

- measurement.

- presentation and disclosure.

What is a purpose of having a conceptual framework?

What is meant by conceptual framework?

A conceptual framework includes one or more formal theories (in part or whole) as well as other concepts and empirical findings from the literature. It is used to show relationships among these ideas and how they relate to the research study.

Why do we need a conceptual framework for financial reporting?

As the purpose of financial reporting is to provide useful information as a basis for economic decision making, a conceptual framework will form a theoretical basis for determining how transactions should be measured (historical value or current value) and reported – ie how they are presented or communicated to users.

What is the importance of writing the conceptual framework?

Defining The Conceptual Framework Shows the reader how different elements come together to facilitate research and a clear understanding of results. A tool (linked concepts) to help facilitate the understanding of the relationship among concepts or variables in relation to the real-world.

What is a benefit of having a conceptual framework?

The credibility of financial reporting is enhanced when objectives and concepts are used to provide direction and structure to financial accounting and reporting. The framework helps by leading to the development of standards that are not only internally consistent but also consistent with each other.

What is conceptual framework sample?

A conceptual framework is an analytical tool that is used to get a comprehensive understanding of a phenomenon. It can be used in different fields of work and is most commonly used to visually explain the key concepts or variables and the relationships between them that need to be studied.