Is deferred compensation considered community property?

California is a community property state. Retirement benefits are a form of deferred compensation for labor expended during the years of employment. These benefits, whether or not vested at the time of divorce, are community property.

Are bonuses included in alimony?

Generally, the court will consider any regularly occurring bonuses as income, subject to the child support guidelines just as wage earnings are. Similarly, for spousal support or property division purposes, regularly occurring bonuses, especially when they are substantial, may be included in the calculation.

How is deferred compensation divided in a divorce?

In most cases, a qualified deferred compensation account such as a 401(k) plan is considered marital property. If the spouse owned the account before marriage, the pre-marital value of the account might be subtracted from the current value of the account before the account is divided.

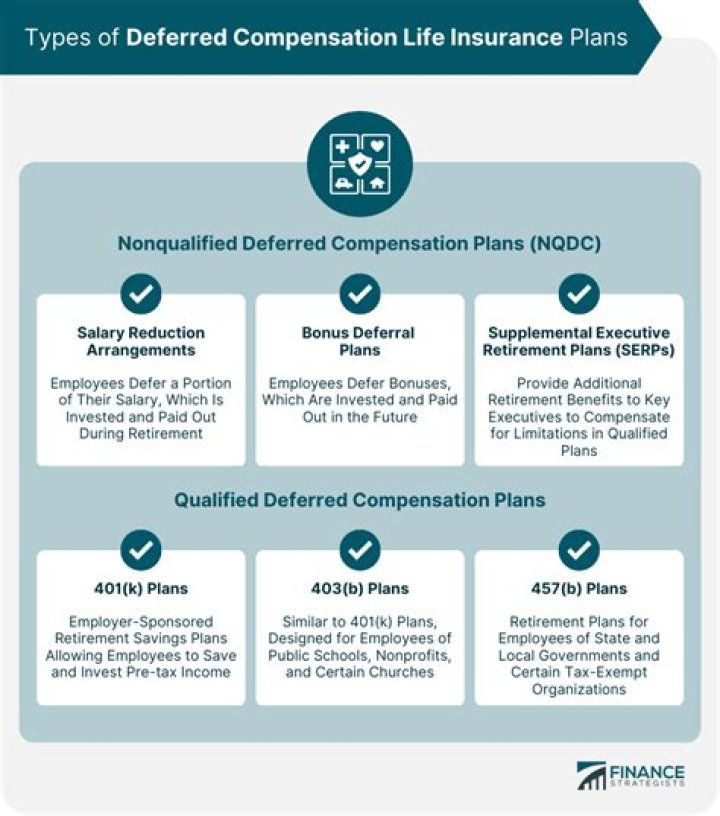

Is deferred compensation an asset?

Deferred compensation plans delay employee compensation until a later date. The assets held for these plans are used to compensate employees in the future, not to generate profits for the company. On the balance sheet, these securities are unmarked and bundled in the line item “Other Assets”.

How does community property affect taxes?

Community property laws affect how you figure your income on your federal income tax return if you are married, live in a community property state or country, and file separate returns. If you are married, your tax usually will be less if you file married filing jointly than if you file married filing separately.

Is alimony calculated on gross or net income?

Alimony serves to help the spouse maintain a comparable standard of living. Alimony calculation uses gross income because this represents the standard of living the parties lived prior to the divorce.

Does deferred compensation count as earned income?

Generally speaking, the tax treatment of deferred compensation is simple: Employees pay taxes on the money when they receive it, not necessarily when they earn it. The year you receive your deferred money, you’ll be taxed on $200,000 in income—10 years’ worth of $20,000 deferrals.

When is deferred compensation considered ” source income “?

“However, if the employee has elected to take the deferred compensation payments over a period of 10 years or more, the deferred compensation payments are taxed in the state of residence when the payments are made.”

Do you have to pay taxes on deferred compensation?

Deferred compensation distributions from non-qualified deferred compensation plans – income deferred from a prior year. While it would have counted in the year it was earned, it does not count when the receipt of the income is postponed to a later year.

How much deferred compensation is not subject to FICA?

For the 2019 tax year, earnings subject to the Social Security portion of FICA were capped at $132,900. Thus, $42,100 of total compensation for the year is not subject to the FICA tax. When the deferred compensation is paid out, say in retirement, no FICA tax will be deducted.

How is deferred compensation set off for the sole benefit of the recipient?

Qualifying deferred compensation is set off for the sole benefit of its recipients, meaning that creditors cannot access the funds if the company fails to pay its debts. Contributions to these plans are capped by law.