Is depreciation constant in straight line method?

The straight-line method of depreciation assumes a constant rate of depreciation.

When should Straight line depreciation be used?

It is used when there no particular pattern to the manner in which the asset is being used over time. Since it is the easiest depreciation method to calculate and results in the fewest calculation errors, using straight line depreciation to calculate an asset’s depreciation is highly recommended.

How is the straight line method of depreciation calculated?

Straight-line depreciation is a simple method for calculating how much a particular fixed asset depreciates (loses value) over time. The straight-line method of depreciation assumes a constant rate of depreciation. It calculates how much a specific asset depreciates in one year, and then depreciates the asset by that amount every year after that.

Which is the best way to depreciate an asset?

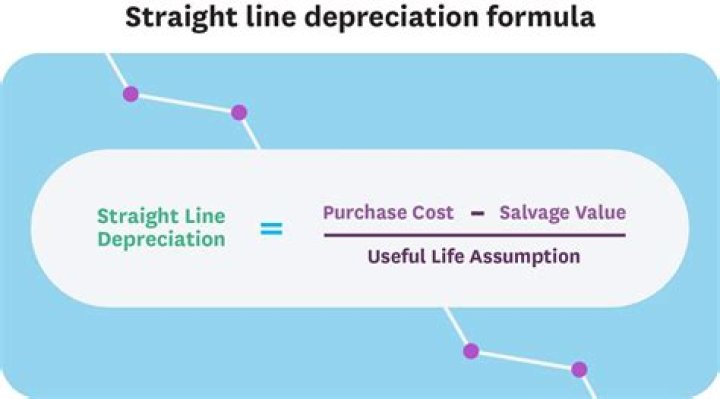

Straight Line Depreciation Straight line depreciation is the most commonly used and easiest method for allocating depreciation of an asset. With the straight line method, the annual depreciation expense equals the cost of the asset minus the salvage value, divided by the useful life (# of years). This guide has examples, formulas, explanations

What are the different methods of depreciation in dynamics?

There are eight methods of depreciation available: Use this method for assets that are not subject to depreciation, for example, land. You must enter depreciation in the fixed asset G/L journal. The Calculate Depreciation batch job omits fixed assets that use this depreciation method.

How is depreciation calculated in the fixed installment method?

Therefore, an equal amount of depreciation is charged every year throughout the useful life of an asset. After the useful life of the asset, its value becomes nil or equal to its residual value. Thus, this method is also called Fixed Installment Method or Fixed percentage on original cost method.