Is extended term insurance a Nonforfeiture option?

Extended-term insurance is often the default non-forfeiture option. With extended term insurance, the face amount of the policy stays the same, but it is flipped to an extended-term insurance policy.

What is non-forfeiture in insurance?

A non-forfeiture option. (or clause) is a provision included in certain life insurance policies stipulating that the policyholder will not forfeit the value of the policy if the policy lapses after a defined period due to missed premium payments.

What are the non-forfeiture options?

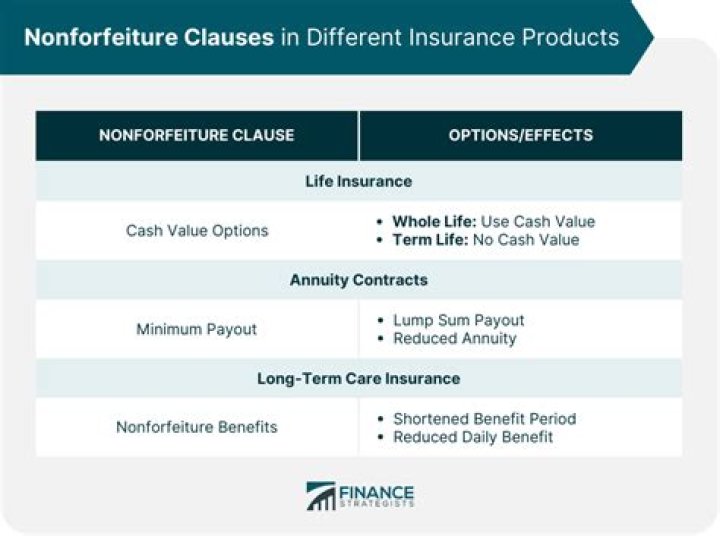

There are three nonforfeiture options: (1) cash surrender; (2) reduced paid- up insurance; and (3) extended term insurance. If a policyowner chooses, he/she may request a cash payment of the cash values when the policy is surrendered.

What is non-forfeiture period?

8) What is the Non-Forfeiture Provision of the Policy? This means that the mentioned benefits would remain available to the Policy Owner under the Non-Forfeiture period even though the Policy Owner may not have paid any due premiums during this period.

What is extended term insurance option?

Extended term insurance is a nonforfeiture option on a whole life policy that uses the policy’s cash value to buy term insurance for the current whole life death benefit for a specified period of time.

What is the benefit of choosing extended term as a Nonforfeiture option quizlet?

What is the benefit of choosing extended term as a nonforfeiture option? It has the highest amount of insurance protection: has the same face amount as the original policy, but for a shorter period of time.

What does extended term insurance mean?

Extended Term Insurance — a nonforfeiture provision in a whole life policy that uses cash value to purchase term insurance equal to the existing amount of life insurance.

What reduced paid-up insurance is as a Nonforfeiture option?

Nonforfeiture Reduced Paid-Up Benefit — a life insurance policy nonforfeiture benefit option to use the cash surrender value of the policy to purchase a fully paid-up life permanent insurance policy for a lesser amount of coverage. Also known as reduced paid-up insurance.

What is an insurance policy’s grace period quizlet?

What is an insurance policy’s grace period? Period of time after the premium is due but the policy remains in force.

Is extended term a dividend option?

The extended term insurance option differs from the reduced paid-up insurance option as it does not allow the policy to continue to earn interest, increase cash value, or pay dividends (if dividends are applicable). It does, however, allow the face amount of the policy to remain the same for a specified period of time.

What is extended life benefit?

A group policy provision that pays a life benefit when (1) the insured is totally and continuously disabled at the time the policy owner stops paying premium until the insured’s death, and (2) if the insured dies within one year of the date the premium payments stopped, or prior to age 65.

What are the three nonforfeiture options?

Non-forfeiture options are ways in which cash values can be paid out to or used in the case the policy is lapsed or surrendered. There are essentially three non-forfeiture options available: cash surrender, reduced paid-up insurance and extended term insurance.

What is extended term insurance?

Extended term insurance is a provision that is sometimes included in the terms of conditions of an insurance policy.

What is extended term option?

An Extended Term Option is one of the standard nonforfeiture options in cash value policies. When a policy owner wants to stop paying required premiums, it is one of the alternatives to surrendering the coverage for its cash value.

What is the extended term insurance option?

Extended term insurance is a nonforfeiture option which may be included with insurance to extend the coverage for a limited period of time upon the failure of a policy-holder to pay the premiums.