Is FIFO A cost flow assumption?

The first in, first out (FIFO) method of inventory valuation is a cost flow assumption that the first goods purchased are also the first goods sold. In most companies, this assumption closely matches the actual flow of goods, and so is considered the most theoretically correct inventory valuation method.

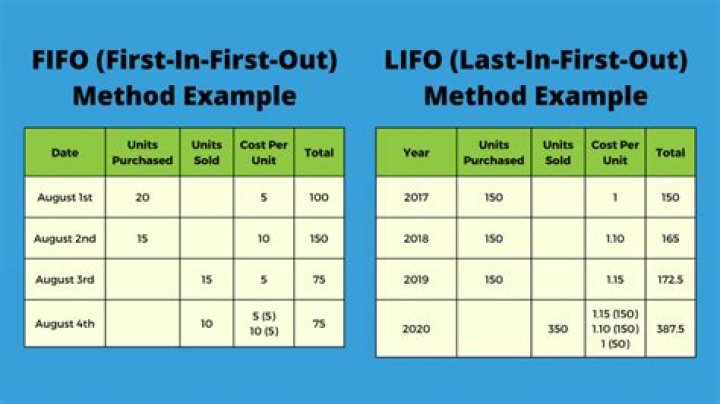

How is FIFO cost flow assumption used?

To calculate FIFO (First-In, First Out) determine the cost of your oldest inventory and multiply that cost by the amount of inventory sold, whereas to calculate LIFO (Last-in, First-Out) determine the cost of your most recent inventory and multiply it by the amount of inventory sold.

What was cost of goods sold using the FIFO cost flow assumption?

FIFO cost flow assumption. Under the first in, first out method, you assume that the first item purchased is also the first one sold. Thus, the cost of goods sold would be $50. Since this is the lowest-cost item in the example, profits would be highest under FIFO.

How does a company determine what cost flow assumption they should use?

In order for a company to use cost flow assumptions in its accounting, it has to balance out costs at the end of the year. The cost of goods sold plus the cost of goods left in inventory must equal the total cost of inventory for the year.

What are the three cost flow assumptions?

In the U.S. the cost flow assumptions include FIFO, LIFO, and average. (If specific identification is used, there is no need to make an assumption.) FIFO, LIFO, average are assumptions because the flow of costs out of inventory does not have to match the way the items were physically removed from inventory.

What are the four cost flow assumptions?

How is inventory cost calculated using FIFO method?

Here is how inventory cost is calculated using the FIFO method: Assume a product is made in three batches during the year. The costs and quantity of each batch are: Batch 1: Quantity 2,000 pieces, Cost to produce $8000. Batch 2: Quantity 1,500 pieces, Cost to produce $7000. Batch 3: Quantity 1,700 pieces, Cost to produce $7700.

How does FIFO affect cost of goods sold?

Under FIFO, the cost of goods sold will be lower and the closing inventory will be higher. However, in times of falling prices, the opposite will hold. 2 . FIFO is the default method of determining inventory value.

How does LIFO accounting work for inventory cost?

LIFO costing (“last-in, first-out”) considers the last produced products as being those sold first. In this case, you would assume that Batch 3 items would be sold first, then Batch 2 items, then the remaining 800 items from Batch 1 would be sold. The total cost of 4000 items sold under LIFO accounting would be $17,906.

When to use specific identification instead of FIFO?

Instead of using FIFO, some businesses use one of these other inventory costing methods : Specific identification is used when specific items can be identified. For example, the cost of antiques or collectibles, fine jewelry, or furs can be determined individually, usually through appraisals.