Is goodwill an amortized?

In 2001, the Financial Accounting Standards Board (FASB) declared in Statement 142–Accounting for Goodwill and Intangible Assets–that goodwill was no longer permitted to be amortized. Goodwill is carried as an asset and evaluated for impairment at least once a year.

Is goodwill amortized over the greater of its estimated life or 40 years?

Goodwill is: Amortized over the greater of its estimated life or 40 years. Only recorded by the seller of a business. The excess of the fair value of a business over the fair value of all net identifiable assets.

What kind of goodwill is amortized?

It is classified as an intangible asset on the balance sheet, since it can neither be seen nor touched. Under US GAAP and IFRS, goodwill is never amortized, because it is considered to have an indefinite useful life.

What does goodwill Amortised mean?

Goodwill amortization refers to the gradual and systematic reduction in the amount of the goodwill asset by recording a periodic amortization charge. This means that the users of a company’s financial statements should be educated about the impact of amortization on reported results.

Is goodwill only recorded by the seller of a business?

From the accounting perspective, business goodwill is generally recorded only if it is acquired as part of a business purchase. The typical way the accountants handle business goodwill is by subtracting the fair market value of the business’s tangible assets from the total business value.

How do you record amortization of goodwill?

To record annual amortization expense, you debit the amortization expense account and credit the intangible asset for the amount of the expense. A debit is one side of an accounting record. A debit increases assets and expense balances while decreasing revenue, net worth and liabilities accounts.

How does the amortization of goodwill work in accounting?

In accounting, goodwill is accrued when an entity pays more for an asset than its fair value, based on the company’s brand, client base, or other factors. Corporations use the purchase method of accounting, which does not allow for automatic amortization of goodwill. Goodwill is carried as an asset and evaluated for impairment at least once a year.

When does goodwill accrue as an intangible asset?

In accounting, goodwill is accrued when an entity pays more for an asset than its fair value, based on the company’s brand, client base, or other factors. In 2001, a legal decision prohibited the amortization of goodwill as an intangible asset; however, in 2014, parts of this ruling were rolled back.

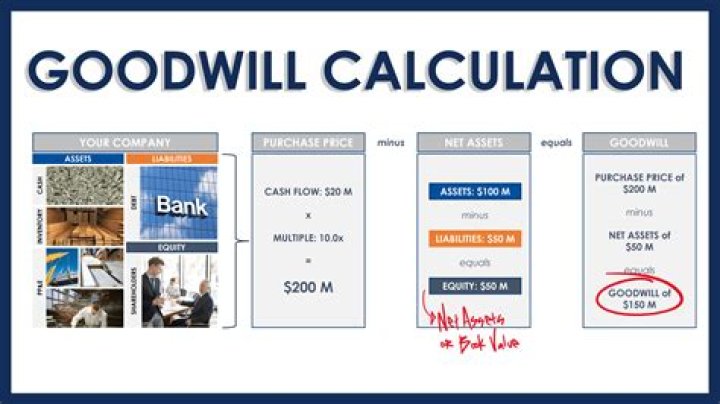

Why does goodwill represent excess of purchase price?

Goodwill represents the excess of purchase price over the fair market value of a company’s net assets: If a business is simply a collection of assets, why would an acquirer pay more than the fair market value of that collection of assets?

When did intangible assets no longer have to be amortized?

In 2001, the Financial Accounting Standards Board (FASB) declared in Statement 142, Accounting for Goodwill and Intangible Assets, that goodwill was no longer permitted to be amortized. In accounting, goodwill is accrued when an entity pays more for an asset than its fair value, based on the company’s brand, client base, or other factors.