Is goodwill consolidated?

Goodwill is treated as an intangible asset in the consolidated statement of financial position. It arises in cases, where the cost of purchase of shares is not equal to their par value.

Is goodwill only Recognised on consolidation?

For a business combination structured by purchasing equity shares of another entity, goodwill is only recognised in the consolidated financial statements. Through the consolidation process, all items within the financial statements of Company S will be combined with those of Company B.

What type of goodwill can be shown on balance sheet?

intangible asset

Goodwill is recorded as an intangible asset on the acquiring company’s balance sheet under the long-term assets account.

Is goodwill on the balance sheet?

Goodwill in accounting is an intangible asset that arises when a buyer acquires an existing business. It is classified as an intangible asset on the balance sheet, since it can neither be seen nor touched. Under US GAAP and IFRS, goodwill is never amortized, because it is considered to have an indefinite useful life.

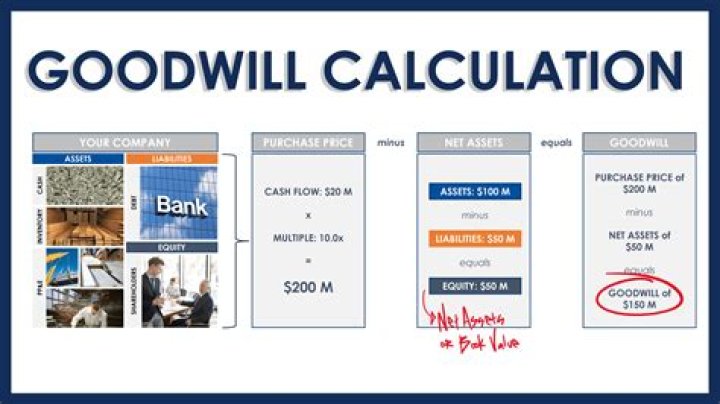

How is consolidated goodwill calculated?

IFRS 3 illustrates the calculation of consolidated goodwill at the date of acquisition as: Consideration paid by parent + non-controlling interest – fair value of the subsidiary’s net identifiable assets = consolidated goodwill.

How will an account of goodwill find out about a consolidated balance sheet?

How does goodwill reduce balance sheet?

The company writes down goodwill by reporting an impairment expense. The amount of the expense directly reduces net income for the year. So a $10,000 goodwill impairment expense means a $10,000 reduction in net income.

Where does goodwill sit on the balance sheet?

Goodwill is located in the assets section of a company’s balance sheet. Unlike physical assets (like buildings and equipment), goodwill is considered an intangible asset.

How is NCI goodwill calculated?

The gross goodwill arising is calculated by matching the fair value of the whole business with the whole fair value of the net assets of the subsidiary to give the whole goodwill of the subsidiary, attributable to both the parent and to the NCI.

How do I prove NCI?

To calculate the NCI of the income statement, take the subsidiaries net income and multiply by the NCI percentage. For example, if the organization owns 70% of the subsidiary and a minority partner owns 30% and subsidiaries net income say $1M. The non-controlling interest would be calculated as $1M x 30% = $300k.

How do you account for negative goodwill on consolidation?

According to Financial Reporting Standard 10, negative goodwill should be recognized and separately disclosed on the balance sheet, immediately below the goodwill heading. It should be recognized in the profit and loss account in the periods in which the non-monetary assets acquired are depreciated or sold.

How do you account for goodwill on a balance sheet?

Subtract the book value from the purchase price to calculate Goodwill. Goodwill is defined as the price paid in excess of the firm’s fair value. To calculate it, simply subtract the total asset market value amount from the purchase price; this amount is nearly always a positive number.

How do you record goodwill on a balance sheet?

Goodwill is recorded when a company acquires (purchases) another company and the purchase price is greater than 1) the fair value of the identifiable tangible and intangible assets acquired, minus 2) the liabilities that were assumed. Goodwill is reported on the balance sheet as a long-term or noncurrent asset.