Is internal rate of return used in capital budgeting?

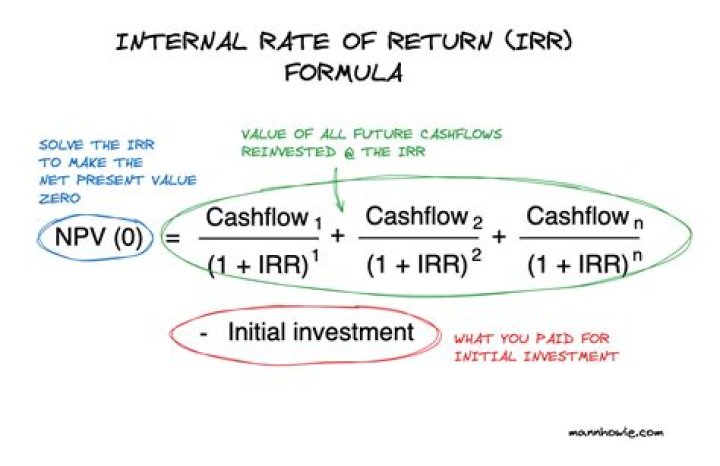

Internal Rate of Return (IRR) is one such technique of capital budgeting. It is the rate of return at which the net present value of a project becomes zero. They call it ‘internal’ because it does not take any external factor (like inflation) into consideration.

Is it better to have a higher or lower IRR?

Generally, the higher the IRR, the better. However, a company may prefer a project with a lower IRR, as long as it still exceeds the cost of capital, because it has other intangible benefits, such as contributing to a bigger strategic plan or impeding competition.

How is internal rate of return used in capital budgeting?

The internal rate of return (IRR) is a metric used in capital budgeting to estimate the profitability of potential investments. The internal rate of return is a discount rate that makes the net present value (NPV) of all cash flows from a particular project equal to zero.

How is the rate of return used in capital planning?

As such, IRR can be used to rank several prospective projects a firm is considering. Assuming all other factors are equal among the various projects, the project with the highest IRR would probably be considered the best and undertaken first. IRR is sometimes referred to as “economic rate of return (ERR)”.

Which is better irr or internal rate of return?

The investment or project with the highest IRR is usually preferred. This easy comparison makes IRR attractive, but there are limits to its usefulness: IRR works only for investments that have an initial cash outflow (the purchase of the investment) followed by one or more cash inflows.

How is IRR used in capital budgeting?

The discount rate often used in capital budgeting that makes the net present value of all cash flows from a particular project equal to zero. Generally speaking, the higher a project’s internal rate of return, the more desirable it is to undertake the project. As such, IRR can be used to rank several prospective projects a firm is considering.