Is it better to refinance with your current mortgage lender?

Mortgage lenders understand that existing borrowers could agree to a higher-than-market rate because it’s lower than the rate they have now. For example, if the lender sees your rate is 4%, you might be offered 3.5% — while a new customer might be quoted just 3%.

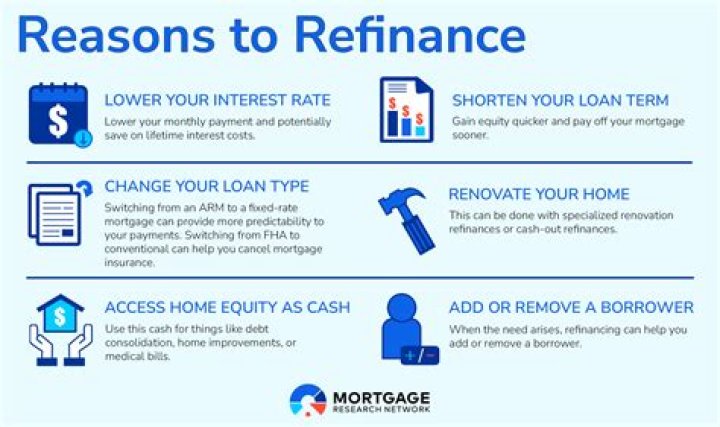

What makes you a good candidate for a refinance?

You’re a good candidate to refinance if you’re planning to stay in your home for a while and are refinancing at a lower interest rate, switching off an adjustable-rate mortgage, or looking to eliminate private mortgage insurance.

How can I lower my mortgage rate without refinancing?

They may be able to offer a competitive rate and cut your closing costs. Ask if they will give you a “ lender credit ” for refinance fees like your appraisal or title report. In very few cases, your lender might be able to lower the rate on your current mortgage without refinancing.

What do I need to get a mortgage refinance?

(Jun 13th, 2021) Before you can request and compare refinance loan offers, you need the right records in hand. Gather these documents: Tax documents from at least the last two years (W-2s if you’re a wage earner, 1040 tax returns with supporting schedules and forms for self-employed or commissioned applicants)

Can you refinance if you have equity in your home?

The amount of equity you have in your current mortgage is a big factor in determining the details of your refinance deal. Whether or not refinancing increases your mortgage amount depends on the new terms and if you are taking additional cash out.

How many people stay with their mortgage company after refinancing?

The latest Mortgage Monitor Report from Black Knight, a leading provider of public property data, shows that just 18% of homeowners in the first quarter of 2019 stayed with their current mortgage company after refinancing. The data cites a refinance market in which competition for your business is rising.

How does the refinancing process for a home work?

Here’s how the refinancing process works. When you apply to refinance, your lender asks for all the same information you gave them when you bought the home. They’ll look at factors like your income, assets, debt and credit to determine whether you can pay back the loan.

Do you have to pay off your mortgage when you refinance?

Whether you are refinancing with your current mortgage lender or a new one, the payoff is required; and mortgage payoff are among the most misunderstood components of a refinance. It’s common for borrowers to confuse their current mortgage balance as shown on a recent statement with their mortgage loan payoff. These are two different figures.