Is standby letter of credit a financial guarantee?

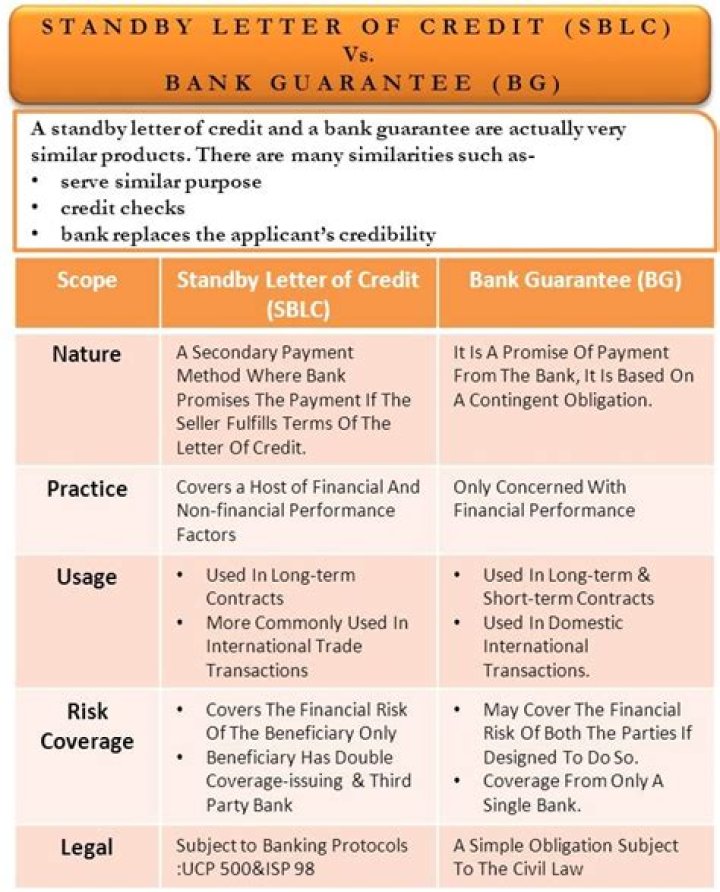

The standby letter of credit is majorly used in long-term contracts. It provides a guarantee to the beneficiary that he will get paid if he performs as per the clauses of the standby letter of credit. In contrast, a bank guarantee is equally used in both domestic as well as international transactions.

Do insurance companies issue letters of credit?

In an insurance contract, carriers typically require the insured company to provide collateral as a guaranteed source of funds, with three of the most commonly accepted forms being letters of credit (LOC), marketable securities and cash.

What is a guarantee standby letter of credit?

A Standby Letter of Credit (SBLC) is a guarantee of payment issued by a bank on behalf of a client that is used as “payment of last resort” should the client fail to fulfill a contractual commitment with a third party.

Can a standby letter of credit be Cancelled?

An irrevocable letter of credit cannot be canceled, nor in any way modified, except with the explicit agreement of all parties involved: the buyer, the seller, and the issuing bank.

What is the difference between Standby LC and guarantee?

Just like Standby LC, a bank guarantee protects the seller but at the same time, it also protects the buyer. While in the case of Standby LCs, only sellers are protected by the issuing bank.

What is the difference between Standby LC and bank guarantee?

Just like Standby LC, a bank guarantee protects the seller but at the same time, it also protects the buyer. While in the case of Standby LCs, only sellers are protected by the issuing bank. While on the other hand, BG only covers financial performance such as the sale of goods, etc.

What is an alternative to a letter of credit?

One alternative to the letter of credit is Purchase Order Financing. This process – sometimes linked to factoring – is where a finance company pays an advance on the order on your behalf, on the basis that it will collect the money directly out of your fee for that big order.

When a non bank issues a letter of credit?

As a result, although there is no affirmative rule in the UCP prohibiting entities that are not banks from issuing, confirming, paying, negotiating, or advising letters of credit, its vocabulary (“issuing bank”, “confirming bank”, etc.) assumes that these entities are banks.

Why was the standby letter of credit created?

However when a bank issues a SBLC on the request of a business, it proves that business’ credit quality and repayment abilities to some extent. The Standby Letter of Credit was created in the United States to circumvent US banking legislation that prohibits banks from issuing guarantees and surety bonds.

Is there a service fee for a standby letter of credit?

The bank will charge a service fee of 1% to 10% for each year when the financial instrument remains valid. If the buyer meets its obligations in the contract before the due date, the bank will terminate the SBLC without a further charge to the buyer.

What does a standby letter of Credit ( SLOC ) guarantee?

The performance SLOC, which is less common, guarantees that the client will complete the project outlined in a contract. The bank agrees to reimburse the third party in the event that its client fails to complete the project.

How does a performance letter of credit ( SBLC ) work?

Performance SBLC A performance-based SBLC guarantees the completion of a project within the scheduled timelines. If the bank’s client is unable to complete the project outlined in the contract, then the bank promises to reimburse the third party to the contract a specific sum of money.