Is Statement of Cash Flows Operating activities?

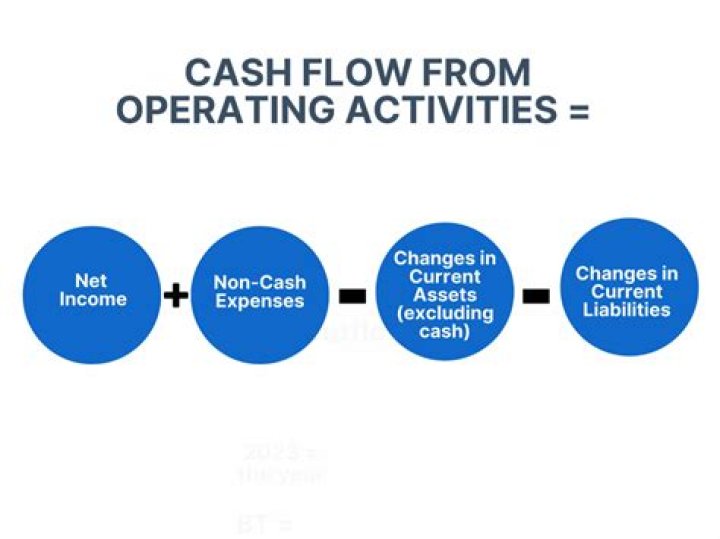

Cash flows from operating activities is a section of a company’s cash flow statement that explains the sources and uses of cash from ongoing regular business activities in a given period. This typically includes net income from the income statement, adjustments to net income, and changes in working capital.

What is included in operating activities on the cash flow statement?

Operating activities include generating revenue. Revenue (also referred to as Sales or Income), paying expenses, and funding working capital. It is calculated by taking a company’s (1) net income. While it is arrived at through, (2) adjusting for non-cash items, and (3) accounting for changes in working capital.

What makes up the statement of cash flows?

As described above, the statement of cash flows consists of three sections. These are briefly explained below: Operating activities section shows cash flows that arise from operating activities of the company. Operating activities include principle revenue generating activities plus other activities that are not investing and financing activities.

Where do you find operating cash flow on a balance sheet?

Operating cash flow, or cash flow from operations (CFO), can be found in the cash flow statement, which reports the changes in cash versus its static counterparts: the income statement, balance sheet, and shareholders’ equity statement.

Why are dividends classified as operating activities in the statement of cash flows?

Interest received and dividends received can be classified as either: an operating activities, or an investing activities, because they represent returns on investment. Some people prefer to classify them under operating activities, because they contribute to the operating profit before taxation.

How is indirect method used in statement of cash flows?

The indirect method can more accurately be described as a reconciliation of net income to cash flows, with all the reconciling items listed out in separate categories which are cash flows from operations, cash flows from investing activities, and cash flows from financing activities.