Should construction interest be capitalized?

Construction interest that is incurred on the construction of a structure intended for rental or business use is not deductible at the time that it is paid. This type of interest is added to the cost basis of the asset instead. For this reason, it is also known as capitalized interest.

Why do you capitalize interest on construction projects?

Understanding Capitalized Interest Because many companies finance the construction of long-term assets with debt, Generally Accepted Accounting Principles (GAAP) allow firms to avoid expensing interest on such debt and include it on their balance sheets as part of the historical cost of long-term assets.

Can interest be Capitalised?

Capitalized interest is interest that is added to the total cost of a long-term asset or loan balance. This makes it so the interest is not recognized in the current period as an interest expense. Capitalized interest appears on the balance sheet rather than the income statement.

What should be capitalized in construction?

Projects such as building construction included in the fixed asset value of the building, the cost of professional fees (architect and engineering), permits and other expenditures necessary to place the asset in its intended location and condition for use should be capitalized.

What is the difference between capitalized interest and accrued interest?

As already outlined, capitalized interest is a term of interest used on a business’s financial statements. The amount of capitalized interest is the amount of accrued interest on the compound interest owed; an accrued amount is the portion of interest that hasn’t been paid since the last payment.

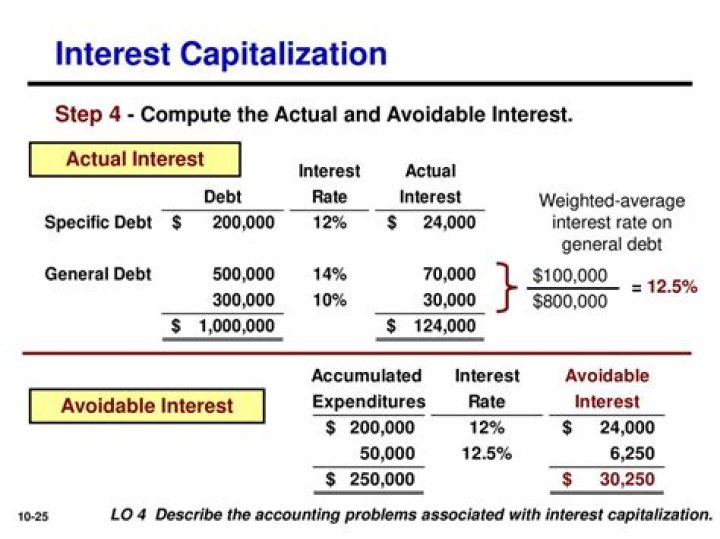

How do you calculate capitalized interest on a construction project?

You can use a capitalized interest calculator, but the formula for figuring interest capitalization is straightforward. Multiply the average amount borrowed during the time it takes to acquire the asset by the interest rate and the development time in years.

How is interest capitalized in the construction of an asset?

Capitalized interest is the cost of the funds used to finance the construction of a long-term asset that an entity constructs for itself. The capitalization of interest is required under the accrual basis of accounting, and results in an increase in the total amount of fixed assets appearing on the balance sheet. Click to see full answer

What kind of costs are capitalized during construction?

What costs are capitalized during construction? Capitalized costs typically arise in relation to the construction of buildings, where most construction costs and related interest costs can be capitalized. Examples of capitalized costs include: Materials used to construct an asset. Sales taxes related to assets purchased for use in a fixed asset.

When do you not have to capitalize interest cost?

When to capitalize interest cost. However, if there is a significant additional accounting and administrative cost associated with capitalizing interest cost, and the benefit of the additional information is minimal, you do not have to capitalize it.

When to capitalize interest cost on land acquisition?

When to capitalize interest cost. If so, the expenditure to acquire the land qualifies for interest capitalization. If an entity constructs a building on a newly-acquired land parcel, then the interest cost associated with the building should be capitalized as part of the building asset, rather than the land asset.