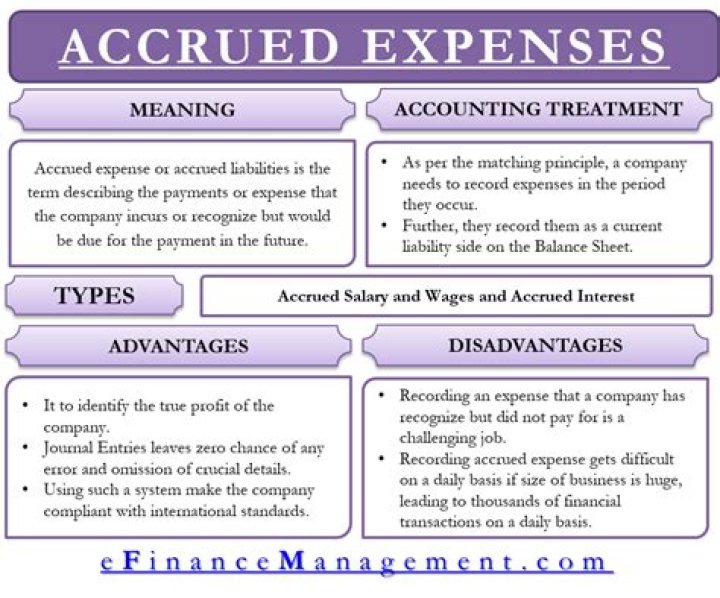

What are accrued expenses?

An accrued expense, also known as accrued liabilities, is an accounting term that refers to an expense that is recognized on the books before it has been paid. Since accrued expenses represent a company’s obligation to make future cash payments, they are shown on a company’s balance sheet as current liabilities.

Are wages accrued expenses?

Accrued payroll includes wages, salaries, commissions, bonuses, and other payroll related expenses that have been earned by a company’s employees, but have not yet been paid or recorded in the company’s general ledger accounts.

What is an accrued expense example?

Examples of accrued expenses include: Utilities used for the month but an invoice has not yet been received before the end of the period. Wages that are incurred but payments have yet to be made to employees. Services and goods consumed but no invoice has been received yet.

Are accrued expenses matched with earnings?

An accrued expense can best be described as an amount a. paid and currently matched with earnings. If, during an accounting period, an expense item has been incurred and consumed but not yet paid for or recorded, then the end-of-period adjusting entry would involve a. a liability account and an asset account.

How do you do accrued expenses?

How to record accrued expenses

- Step 1: You incur the expense. You incur an expense at the end of the accounting period. You owe a debt but have not yet been billed.

- Step 2: You pay the expense. At the beginning of the next accounting period, you pay the expense. Reverse the original entry in your books.

Do you reverse accrued payroll?

Payroll accruals are a common practice when you have payroll cycles that cross different accounting periods. You need to recognize the payroll expenses incurred during the end of the accounting period. Equally important is reversing that accrual when you issue the payroll deposits.