What are qualitative characteristics of useful financial information?

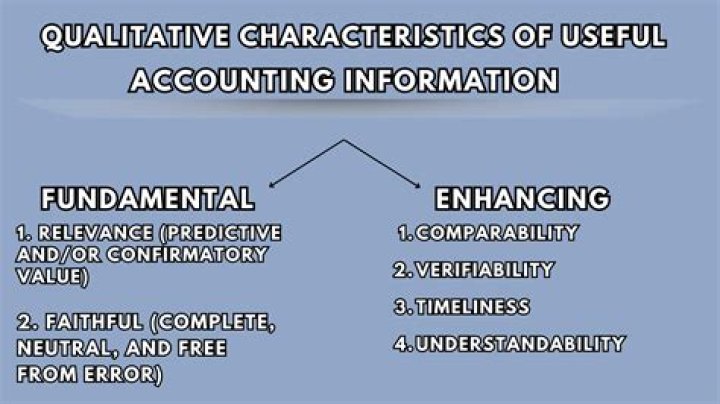

Enhancing qualitative characteristics include comparability, verifiability, timeliness and understandability. Comparability requires financial information to be comparable across periods and companies. Comparability is achieved through consistency.

What are the two essential characteristics of useful financial information?

Primary Decision-Specific Qualities Relevance and reliability are the two primary qualities that make accounting information useful for decision making.

What are the four principal qualitative characteristics of financial statements?

characteristics are the attributes that make the information provided in financial reports useful to users. As figure 1 shows, the four principal qualitative characteristics are understandability, relevance, reliability and comparability (IASB, 2006).

What are the two fundamental qualitative characteristics of financial reporting?

Fundamental Characteristics distinguish useful financial reporting information from that is not useful or misleading. The two fundamental Qualitative characteristics are : Relevance. Faithful Representation.

Why are qualitative characteristics of accounting information important?

The qualitative characteristics of accounting information are important because they make it easier for both company management and investors to utilize a company’s financial statements to make well-informed decisions. certification program for those looking to take their careers to the next level.

Which is an enhancing qualitative characteristic of IFRS?

However, information that is verifiable is generally more decision useful than information that cannot be independently verified; therefore, the boards propose that verifiability should be an enhancing qualitative characteristic.

What are the qualitative characteristics of ACCA FA?

ACCA FA (F3) Notes: B1a. Qualitative characteristics | aCOWtancy Textbook B1a. Qualitative characteristics The IASB’s Conceptual Framework for Financial Reporting describes the basic concepts by which financial statements are prepared.