What are Section 174 deductions?

IRC Section 174 is deceptively simple. It provides, in part: “A taxpayer may treat research or experimental expenditures which are paid or incurred by him during the taxable year in connection with his trade or business as expenses which are not chargeable to capital account.

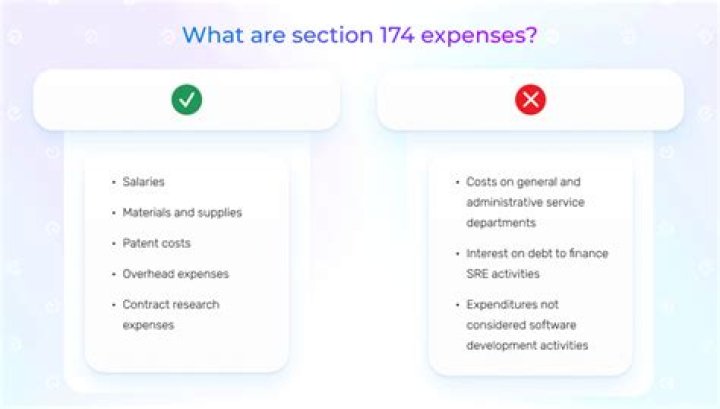

What is a Section 174 expense?

A taxpayer may treat research or experimental expenditures which are paid or incurred by him during the taxable year in connection with his trade or business as expenses which are not chargeable to capital account.

Are S Corp expenses tax deductible?

In general, S corporation losses are always deductible against shareholders’ individual taxable incomes. Ordinary business expenses such as rent, taxes, advertising, company-provided employee benefits, depreciation and interest can be subtracted from profits and income to arrive at the net income for the business.

Can corporations deduct section 212 expenses?

Corporations cannot deduct Section 212 investment expenses, therefore they don’t provide tax relief when a trader does not qualify for trader tax status.

What is the Section 174 test?

The IRC section 174 test requires that the expenditure be incurred in the taxpayer’s trade or business and represent an R&D cost in the experimental or laboratory sense, meaning that the expenditures are incurred for activities intended to discover information that would eliminate uncertainty concerning the development …

Can R&D credit offset AMT?

AMT OFFSET Fortunately, the PATH Act also allows eligible small businesses (ESBs) to use the R&D credit to offset their AMT liability for tax years beginning after Dec. Gross receipts are reduced by returns and allowances and must be annualized for short tax years, and predecessors are taken into account.

Are section 212 expenses deductible 2020?

212, the advisory fees and other investment expenses of the fund are now no longer deductible to fund investors that are individuals or similarly taxed entities, such as trusts.

What is a Section 212 expense?

Section 212 provides that in the case of an individual, there shall be allowed as a deduction all the ordinary and necessary expenses paid or incurred during the taxable year (1) for the production or collection of income, (2) for the management, conservation, or maintenance of property held for the production of …

Why was section 174 created by the IRS?

IRS Clarifies Section 174 Regulations. Section 174 was enacted to encourage taxpayers to conduct research activities by providing certainty about the deductibility of their research expenses. In general, unless a taxpayer elects to defer and amortize its research expenses, Section 174 provides that a taxpayer is entitled to deduct,…

What kind of expenses can you deduct under Section 174?

Only expenses for research and experimentation (“R&E”) are deductible under Section 174. What exactly is R&E?

How are research and experimental expenses amortized under Sec 174?

Although the default method of accounting for research and experimental expenses is to deduct the costs under Sec. 174 in the year they are incurred, taxpayers may instead elect to defer the expenses and amortize them over a period of not less than 60 months (Sec. 174 (b)) or elect to amortize them over a set 10 – year period (Sec. 59 (e)).

What’s the difference between SEC 174 and sec.41?

But herein lies the issue—changes under Sec. 174 are executed on a cutoff, or prospective, basis for expenditures incurred in the year of change and future years only (Sec. 174 (a) (3)).