What are the 3 manufacturing costs?

Manufacturing costs fall into three broad categories of expenses: materials, labor, and overhead.

What are included in manufacturing costs?

Manufacturing costs are the costs incurred during the production of a product. These costs include the costs of direct material, direct labor, and manufacturing overhead. Direct labor is that portion of the labor cost of the production process that is assigned to a unit of production.

Which cost is not part of direct production cost?

Direct costs usually benefit only one cost object. Items that are not direct costs are pooled and allocated based on cost drivers. Direct and indirect costs are the major costs involved in the production of a good or service. While direct costs are easily traced to a product, indirect costs are not.

What are direct costs in manufacturing?

Direct costs are expenses that a company can easily connect to a specific “cost object,” which may be a product, department or project. This can include software, equipment and raw materials. It can also include labor, assuming the labor is specific to the product, department or project.

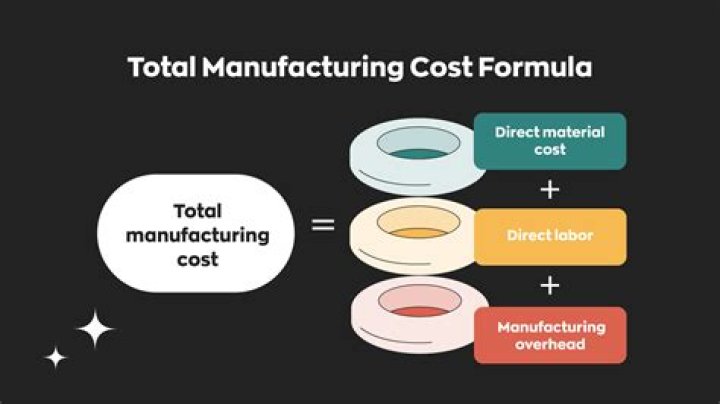

How do you calculate manufacturing costs?

To calculate total manufacturing cost you add together three different cost categories: the costs of direct materials, direct labour and manufacturing overheads. Expressed as a formula, that’s: Total manufacturing cost = Direct materials + Direct labour + Manufacturing overheads.

What are the three elements to consider in manufacturing?

The three elements of manufacturing costs are material, labour, and manufacturing overhead.

What are the two standard components of manufacturing costs?

The two standard components of manufacturing costs are standard price and standard quantity.

How do you calculate direct manufacturing labor cost?

The labor cost per unit is obtained by multiplying the direct labor hourly rate by the time required to complete one unit of a product. For example, if the hourly rate is $16.75, and it takes 0.1 hours to manufacture one unit of a product, the direct labor cost per unit equals $1.68 ($16.75 x 0.1).