What are the 3 primary inventory costing methods?

The method a company uses to determine it cost of inventory (inventory valuation) directly impacts the financial statements. The three main methods for inventory costing are First-in, First-Out (FIFO), Last-in, Last-Out (LIFO) and Average cost.

What inventory method does General Motors use?

General Motors and Ford use the last-in, first-out (LIFO) method to value their inventories.

What is inventory estimation method?

The gross profit method estimates the value of inventory by applying the company’s historical gross profit percentage to current‐period information about net sales and the cost of goods available for sale. Gross profit equals net sales minus the cost of goods sold.

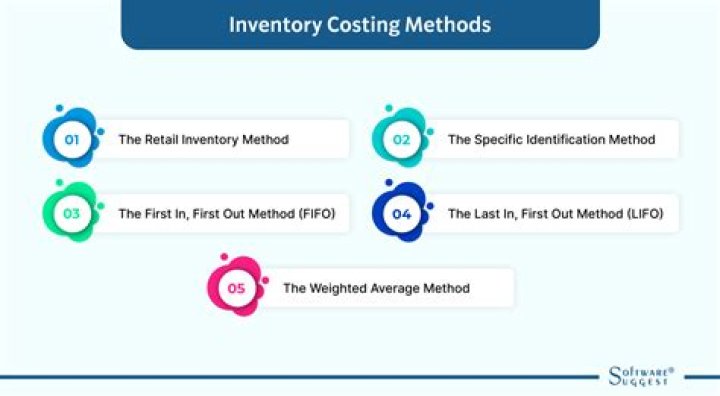

What are the four main inventory valuation methods?

Below, we break down the four most common methods, and the pros and cons of each.

- WAC (weighted average cost) The WAC method of inventory valuation uses a weighted average to determine the amount that goes into COGS and inventory.

- Specific identification method.

- FIFO (first-in, first-out)

- LIFO (last-in, first-out)

What is the purpose of inventory estimation?

Inventory valuation is done at the end of every financial year to calculate the cost of goods sold and the cost of the unsold inventory. This is crucial as the excess or shortage of inventory affects the production and profitability of a business.

Which is the best method for estimating inventories?

Two ways of estimating inventory levels are the gross profit method and the retail inventory method. Gross profit method. The gross profit method estimates the value of inventory by applying the company’s historical gross profit percentage to current‐period information about net sales and the cost of goods available for sale.

How are inventories calculated in the perpetual system?

Estimating Inventories. Companies using the perpetual system simply report the inventory account balance in such situations, but companies using the periodic system must estimate the value of inventory. Two ways of estimating inventory levels are the gross profit method and the retail inventory method.

How are cost of goods sold and inventories calculated?

Estimating Inventories. Alternatively, cost of goods sold may be determined by multiplying net sales by 65% (100% – gross profit margin of 35%). Finally, the estimated cost of goods sold is subtracted from the cost of goods available for sale to estimate the value of inventory.

How is inventory destroyed by a fire estimated?

The inventory destroyed by fire can be estimated via the gross profit method, as shown. A method that is widely used by merchandising firms to value or estimate ending inventory is the retail method.