What are the 4 accounting process?

First Four Steps in the Accounting Cycle. The first four steps in the accounting cycle are (1) identify and analyze transactions, (2) record transactions to a journal, (3) post journal information to a ledger, and (4) prepare an unadjusted trial balance.

What is the most important step in accounting process?

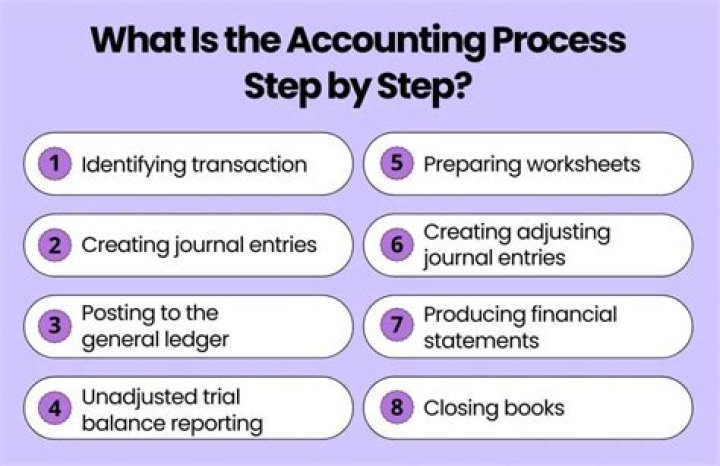

The 8 Steps of the Accounting Cycle

- Step 1: Identify Transactions.

- Step 2: Record Transactions in a Journal.

- Step 3: Posting.

- Step 4: Unadjusted Trial Balance.

- Step 5: Worksheet.

- Step 6: Adjusting Journal Entries.

- Step 7: Financial Statements.

- Step 8: Closing the Books.

Which is the next step in the accounting cycle?

: With the transactions set in place, the next step is to record these entries in the company’s journal in chronological order. In debiting one or more accounts and crediting one or more accounts, the debits and credits must always balance.

When does the closing process take place in accounting?

The closing process takes place at the (end/beginning) of an accounting period, after the (adjusted/unadjusted) trial balance is prepared and (after/before) the financial statements are prepared. end, adjusted, after

What are journal entries in the accounting cycle?

Journal Entries Guide Journal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits). Without proper journal entries, companies’ financial statements would be inaccurate and a complete mess.

What are the four basic phases of accounting?

There are four basic phases of accounting: recording, classifying, summarizing and interpreting financial data. Communication may not be formally considered one of the accounting phases, but it is a crucial step as well. All accounting information should be communicated properly to the appropriate parties after analyzing.