What are the assertions in audit?

The different financial statement assertions attested to by a company’s statement preparer include assertions of existence, completeness, rights and obligations, accuracy and valuation, and presentation and disclosure.

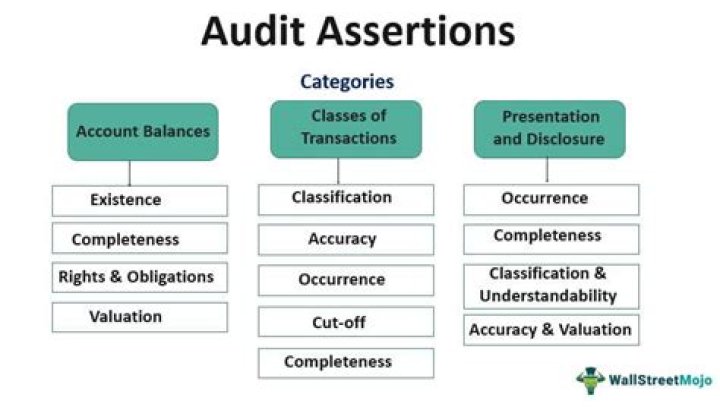

What are the five audit assertions?

The five (or seven) assertions are the following:

- Occurrence or Existence.

- Completeness.

- Allocation or Valuation.

- Rights and Obligations.

- Presentation and Disclosure.

What are significant risks in auditing?

Significant risk – An identified and assessed risk of material misstatement that, in the auditor’s judgment, requires special audit consideration. Now special consideration is required. if likelihood / probability of misstatement is very high and Amount involved is all high.

What is a significant audit area?

A significant audit area is one that contains a significant transaction class, material account balance, or fraud or other significant risk or requires significant disclosures. An Assessed Risk of Material Misstatement is computed for you in the last column.

What are the 5 types of assertion?

There are five types of assertion: basic, emphatic, escalating, I-language, and positive. A basic assertion is a straightforward statement that expresses a belief, feeling, opinion, or preference.

What does an audit plan include?

Audit Plan The planned nature, timing, and extent of the risk assessment procedures; The planned nature, timing, and extent of tests of controls and substantive procedures;12 and. Other planned audit procedures required to be performed so that the engagement complies with PCAOB standards.

How materiality is applied in an audit?

The concept of materiality is applied by the auditor both in planning and performing the audit, and in evaluating the effect of identified misstatements on the audit and of uncorrected misstatements, if any, on the financial statements and in forming the opinion in the auditor’s report.

How can audit risk be reduced?

In this case, the auditor can reduce audit risk by:

- Perform proper audit planning before executing audit procedures.

- Design suitable audit procedures that respond to the assessed risk.

- Properly allocate staff based on their skills and experiences.

- Have proper monitoring and supervision of audit work.