What are the factors that influence the reliability of audit evidence?

The six characteristics of reliability that determine the evidence are independence of provider, effectiveness of clients internal controls, auditors direct knowledge, qualifications of individuals providing the information, degree of objectivity and timeliness.

What are the types of audit evidence?

The auditor can obtain different types of audit evidence, and it includes Physical Examination, documentation, analytical procedure, observations, confirmations, inquiries, etc.

What are sources of audit evidence?

Internal sources of audit evidence include a company’s documented processes, policy documents, accounting records, invoices, system logs, and reports. External sources of audit evidence can include information from banks, debtors, suppliers, stock exchanges, and the Internal Revenue Service.

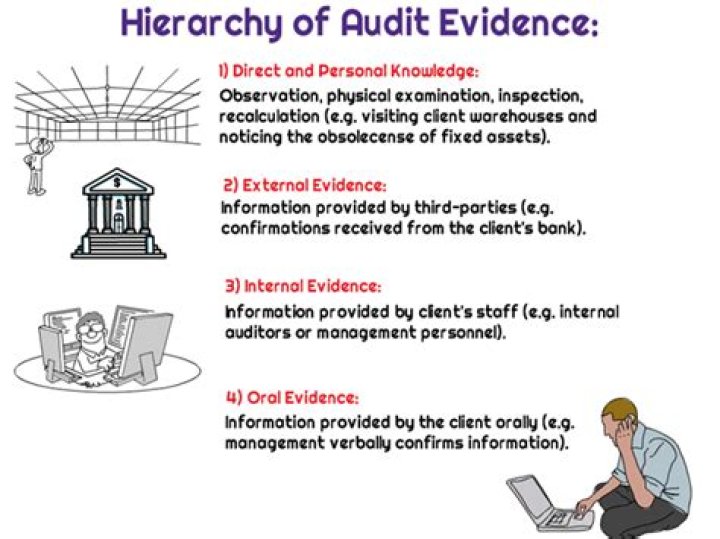

What is reliability of evidence?

The reliability of evidence refers to the degree to which evidence is considered believable or trustworthy. One factor is the independence of the provider (evidence obtained from a source outside the client company is more reliable than that obtained within).

What is the most reliable audit evidence?

Audit evidence is more reliable when it exists in documentary form, whether paper, electronic, or other medium (for example, a contempo- raneously written record of a meeting is more reliable than a subse- quent oral representation of the matters discussed). audit evidence provided by photocopies or facsimiles.

What are the qualities of audit evidence?

Appropriateness is the measure of the quality of audit evidence, i.e., its relevance and reliability. To be appropriate, audit evidence must be both relevant and reliable in providing support for the conclusions on which the auditor’s opinion is based.

How does the quantity of audit evidence affect the quality of evidence?

Likewise, the quantity of audit evidence will be influenced by the risk of material misstatement of financial statements and the quality of evidence obtained. First, the number of audit evidence that auditors need to obtain will directly link to the risk of material misstatement.

Which is the best example of appropriate audit evidence?

This is why the concept of appropriate audit evidence is usually linked to the context of reliable audit evidence. For example, the auditors’ generated evidence, such as recalculation working, is usually considered to be the audit evidence of the highest quality.

When do auditors have enough evidence on file?

However, when determining whether they have enough evidence on file the auditor must consider: the reliability of the evidence obtained. Consider, for example, the audit of a bank balance: Auditors will confirm year-end bank balances directly with the bank.

What makes an audit opinion a trustworthy opinion?

They must consider evidence gathered by both the defence and the prosecution and then, based upon the evidence presented, reach a conclusion. Similarly, in order for the auditor’s opinion to be considered trustworthy it must be based upon more than simple judgement and gut feeling.