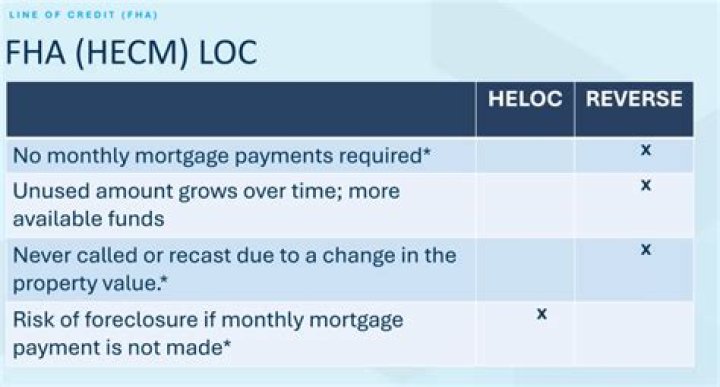

What are the hidden dangers of a reverse mortgage?

Reverse mortgage contracts can have hidden costs such as fees and interest can eat up your home equity. Unless you are careful, you can risk losing your home or have it passed on to the lender when you die instead of to your heirs.

Do reverse mortgages make sense?

And as you suggest, a reverse mortgage could also make sense, provided you understand exactly what you’re getting into and how it ties into your larger financial picture. On the plus side, a reverse mortgage will allow you to tap into a portion of your home’s equity without having to make monthly payments.

What’s the pros and cons of reverse mortgage?

The money is tax free. Rather than income earned, a reverse mortgage is considered a loan so the IRS can’t get its sticky fingers on it. And a reverse mortgage will not affect your Social Security or Medicare payments. As for the cons, failing to keep up with the monthly fees has cost a lot of people their homes.

What’s the catch with reverse mortgages?

A reverse mortgage does not guarantee financial security for the rest of your life. You don’t receive the full value of loan. The face amount will be slashed by higher-than-average closing costs, origination fees, upfront mortgage insurance, appraisal fees and servicing fees over the life of the mortgage.

What makes a reverse mortgage a good idea?

At first blush, a reverse mortgage, also known as a home equity conversion mortgage, sounds like a great idea: You continue to live in your home without having to make any mortgage payments, and at the same time receive a lump sum of cash to be used for whatever you like.

Do you have to pay mortgage insurance on a reverse mortgage?

Since you’re not making a down payment on a reverse mortgage, you pay the premium on mortgage insurance. The premium equals 0.5% if you take out a loan equal to 60% or less of the appraised value of the home. The premium jumps to a whopping 2.5% if the loan totals more than 60% of the home’s value.

Can you live outside your home with a reverse mortgage?

The terms of a reverse mortgage require you to live in the property as your primary residence. If you are already in poor health and are looking into possible long term care in the near future, a reverse mortgage may be the wrong choice for you as your loan wouldn’t allow you to be living outside the home for a period of more than 12 months.

Can a reverse mortgage be repaid if the value of the home exceeds the loan balance?

Because of the reverse mortgage’s non-recourse feature, the homeowners or their heirs will never owe more than 95% of the home’s appraised value, even if the balance of the loan exceeds this amount. This means that if the home appraises for less than the loan balance, 95% of that amount is all that needs to be repaid.