What are the limitations of going concern concept?

The disadvantages of going concern concept are: In case there are chances when the business may wind up because of the non demand of the product in the market or any other factor then in such a case the financial statements that are prepared on going concern cases may depict the wrong information.

What is the purpose of going concern?

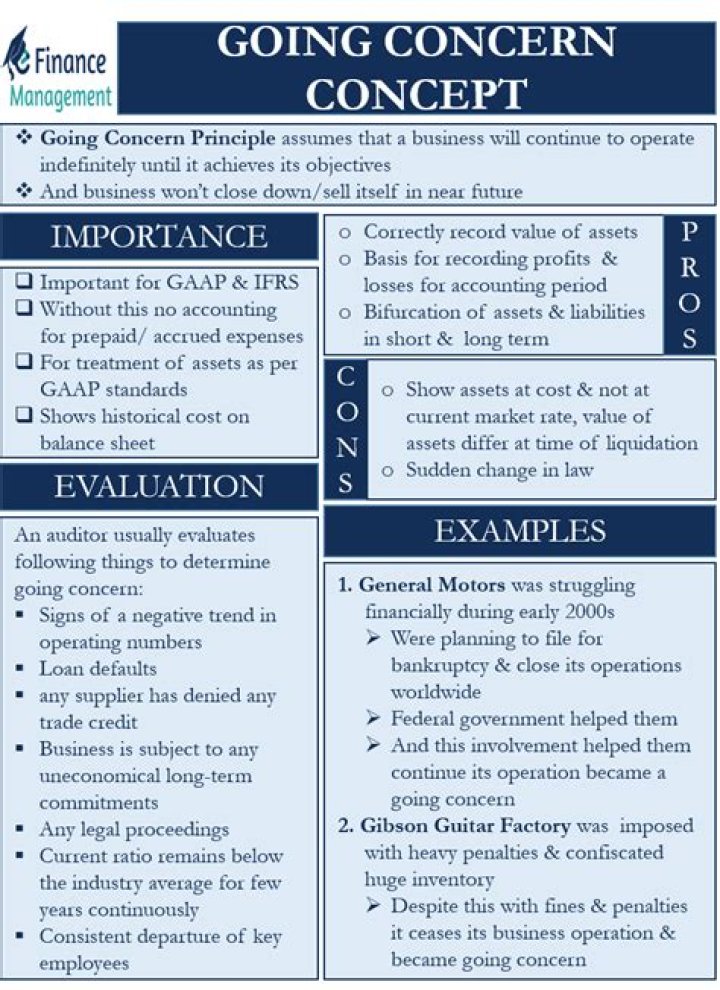

What Is Going Concern? Going concern is an accounting term for a company that has the resources needed to continue operating indefinitely until it provides evidence to the contrary. This term also refers to a company’s ability to make enough money to stay afloat or to avoid bankruptcy.

What is a going concern concept?

Going concern is one of the very fundamental principles of accounting. It assumes that the entity will continue to remain in business for the foreseeable future. Conversely, it also means that the entity does not plan to, or expect to be forced to, liquidate its assets.

What is going concern concept one example?

An example of the application of going concern concept of accounting is the computation of depreciation on the basis of expected economic life of fixed assets rather than their current market value. Another example of the going concern assumption is the prepayment and accrual of expenses.

How is going concern concept applied?

The going concern concept is a fundamental principle of accounting. It assumes that during and beyond the next fiscal period a company will complete its current plans, use its existing assets and continue to meet its financial obligations. This underlying principle is also known as the continuing concern concept.

What is going concern concept with example?

A company is a going concern if no evidence is available to believe that it will or will have to cease its operations in foreseeable future. Another example of the going concern assumption is the prepayment and accrual of expenses.

How do you prove going concern?

How to Assess Going-Concerns

- Current ratio: Divide current assets by current liabilities to get the current ratio.

- Debt ratio: Total liabilities divided by total assets provides the company’s debt ratio.

- Net income to net sales: This ratio measures how well the company is managing its expenses.

What is the opposite of a going concern?

A going concern is a company that is currently operating and is also making a profit. A company that is not a going concern has gone bankrupt and liquidated its assets. The opposite of a going concern or profitable company may also be an unprofitable company.

Why is the going concern concept so important?

The going concern concept of accounting is of great importance for accountants because if a company is a going concern, it must prepare its financial statements in accordance with applicable financial reporting framework such as generally accepted accounting principals applicable in United States of America (US-GAAP) and international financial …

What happens if there is a going concern assumption?

If the financial statements of the enterprise, which are likely to get shut down in the future, are prepared based on the going concern assumption, then the truth and fairness of the financial accounts are hampered. It misleads the investors as the firm may get closed after the preparation and publications of financial statements.

Which is an example of the going concern principle?

The sound basis for the measurement of income or the profit is provided by the going concern principle. Due to this, the product that can be used in the business for more than a year or having future economic benefits is recognized as a fixed asset, not as an expense.

What makes a company a ” going concern ” in accounting?

The going concern is one the accounting assumptions wherein the financial statements of the companies are prepared on the basis that the company will continue its working in anticipated future and has no intention or need to close materially its operations.