What are the problems with the discounted cash flow model?

There are a number of inherent problems with earnings and cash flow forecasting that can generate problems with DCF analysis. The most prevalent is that the uncertainty with cash flow projection increases for each year in the forecast—and DCF models often use five or even 10 years’ worth of estimates.

What are the problems associated with using the discounted payback period to evaluate cash flows?

What are the problems associated with using the discounted payback period to evaluate cash flows? Ignores the time value of money, requires an arbitrary cutoff point, ignores cash flows beyond the cutoff date, biased against long-term projects, such as research and development, and new projects.

What are the advantages disadvantages of using the discounted cash flows method of estimating the value of a company?

DCF Valuation is extremely sensitive to assumptions related to perpetual growth rate and discount rate. Any minor tweaking here and there, and the DCF Valuation will fluctuate wildly and the fair value so generated won’t be accurate. It works best only when there is a high degree of confidence about future cash flows.

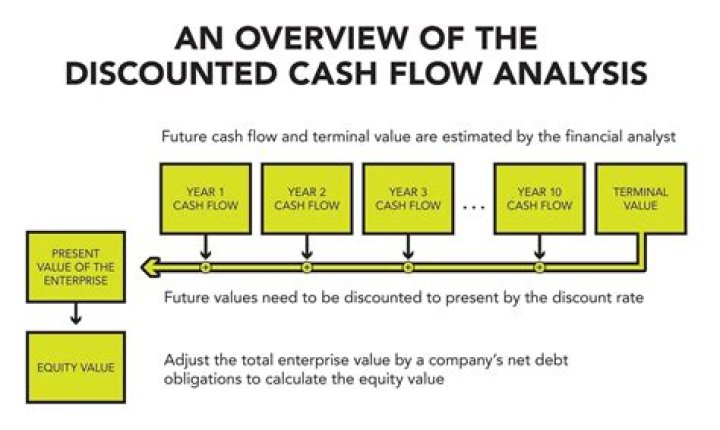

Why do we use discounted cash flow?

Discounted cash flow (DCF) helps determine the value of an investment based on its future cash flows. The present value of expected future cash flows is arrived at by using a discount rate to calculate the DCF. If the DCF is above the current cost of the investment, the opportunity could result in positive returns.

What is the payback decision rule?

The payback method is a decision rule that says a project should only be accepted if the initial investment is recovered within a certain period of time. Accept the project whose pay back period is less than the life of the standard pay back period.

Are there any problems with using growth rate to estimate discount rate?

When choosing a method to estimate the discount rate, there are typically no surefire (or easy) answers. Perhaps the biggest problem with growth rate assumptions is when they are used as a perpetual growth rate assumption. Assuming that anything will hold in perpetuity is highly theoretical.

What are the pitfalls of discounted cash flow analysis?

Small, erroneous assumptions in the first couple years of a model can amplify variances in operating cash flow projections in the later years of the model. Free cash flow projection involves projecting capital expenditures for each model year. Again, the degree of uncertainty increases with each additional year in the model.

What’s the change in the value of my home if I change the discount rate?

Changing only the discount rate to 10% and leaving all other variables the same, the value is $16.21. That’s a 27% change based on a 200 basis point change in the discount rate.

When to use target multiple for discounted cash flow?

Choosing a target multiple range is where it gets tricky. While this is analogous to arbitrary discount rate selection, using a trailing earnings number two years out and an appropriate P/E multiple to calculate a target price will entail far fewer assumptions to “value” the stock than under the DCF scenario.