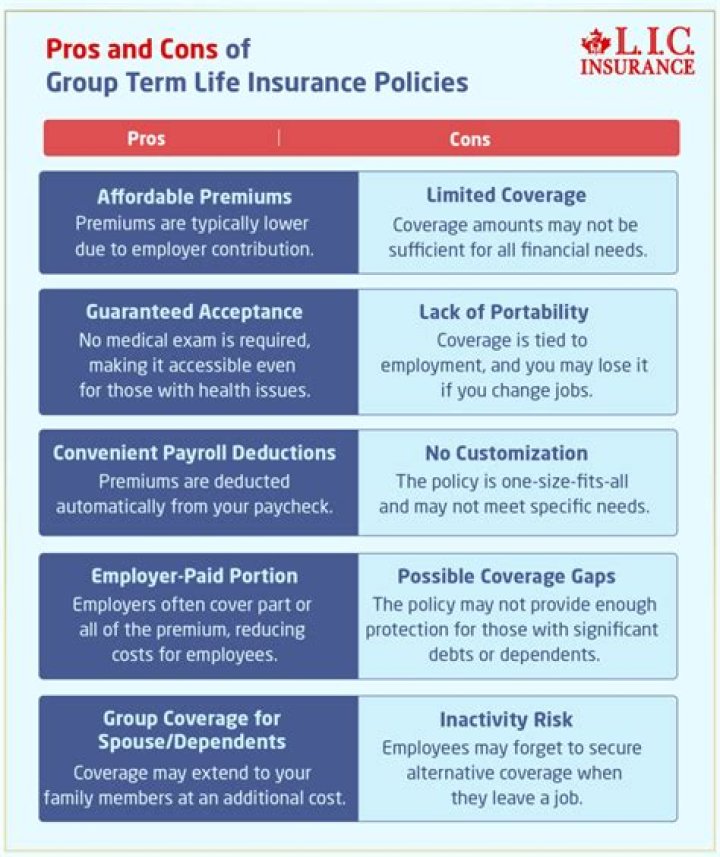

What are the pros and cons of term life insurance?

Term Life Pros & Cons

| Pros | Cons |

|---|---|

| Beneficiaries will receive larger death payouts | Must re-qualify at the end of the term |

| Can be converted to whole life insurance | Difficult to qualify if there is a significant health issue |

| – | Premiums can go up every time you take out a new term |

| – | Policy accumulates no cash value |

What is the difference between whole term and permanent life insurance?

Term life and permanent life are the two main types of life insurance policies. While permanent insurance lasts your entire life, term insurance lasts for a set time period that you choose when you buy a policy — say 10, 20 or 30 years.

What is the catch with whole life insurance?

When you purchase the policy, the premiums will be locked in for the life of the policy as long as you pay them. They will be higher than the premiums of a term life insurance policy because your entire lifetime is built into the calculation. Unlike term insurance, whole life policies don’t expire.

What’s the difference between life insurance and term insurance?

Life insurance plans, on the other hand, are flexible. Traditional life insurance plans promise a paid-up value and a surrender value. You can also avail policy loans under such plans. Moreover, if you choose ULIPs, you can also withdraw partially, switch or pay additional premiums.

How to choose term life or whole life insurance?

Term life vs. whole life: policy features Policy features Term life insurance Whole life insurance Choice of policy length ✓ Provides lifelong coverage ✓ Premium generally stays the same ✓ ✓ Low premium ✓

What are the components of term life insurance?

A term life insurance policy has 3 main components – face amount (protection or death benefit), premium to be paid (cost to the insured), and length of coverage (term).

What happens at the end of term life insurance?

The policy expires at the end of the term. If the insured person dies during the term of the policy, the beneficiary is paid the benefit (face) amount. If the insured person is alive after the term (duration) of the policy, no benefit is paid and the policy expires.