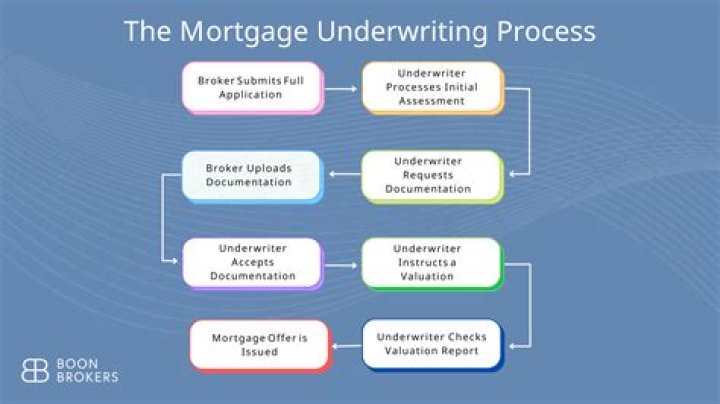

What are the steps of underwriting process?

What exactly is underwriting?

- Step 1: Application Quality Check. Your application is first gone through to make sure the information provided is complete and correct.

- Step2: Medical Examination.

- Step 3: Final Application Rating.

What is the purpose of the underwriting process?

Summary. Underwriting simply means that your lender verifies your income, assets, debt and property details in order to issue final approval for your loan. An underwriter is a financial expert who takes a look at your finances and assesses how much risk a lender will take on if they decide to give you a loan.

What is underwriting explain the process of underwriting?

Underwriting is the process through which an individual or institution takes on financial risk for a fee. Underwriting ensures that a company filing for an IPO will raise the amount of capital needed, and provides the underwriters with a premium or profit for their services.

What’s next after underwriting approval?

The Underwriter issues the Clear To Close (CTC) once all the conditions meet the guidelines. The Closing Department then sends the title company the “loan instructions” so they can prepare the final Closing Disclosure (CD). The final Closing Disclosure (CD) will provide the exact amount of money due at closing.

Why do you need to go through the underwriting process?

The underwriting process is an essential part of any insurance application. When an individual applies for insurance coverage, he or she is essentially asking the insurance company to take on the potential risk of having to pay a claim in the future.

What is the definition of an underwriter?

Definition: Underwriting is one of the most important functions in the financial world wherein an individual or an institution undertakes the risk associated with a venture, an investment, or a loan in lieu of a premium. Underwriters are found in banking, insurance, and stock markets.

What is the definition of an underwriting cycle?

Underwriting cycle refers to fluctuations in the insurance business over a period of time. A typical underwriting cycle spans a number of years, as market conditions for the underwriting business go from boom to bust and back to boom again. Underwriting cycle is also known as “insurance cycle.”.

When does an underwriter need to be involved in appraisal?

Depending on the process and whether a human underwriter is involved, the appraisal process can be almost instant or take a few hours, days, or even weeks. The most common type of loan underwriting that involves a human underwriter is for mortgages and is the type of loan underwriting that most people face during their lifetime.