What are the two methods to prepare a cash flow statement?

There are two ways to prepare a cash flow statement: the direct method and the indirect method: Direct method – Operating cash flows are presented as a list of ingoing and outgoing cash flows. Essentially, the direct method subtracts the money you spend from the money you receive.

When preparing your statement of cash flows using the indirect method we would first add back?

Using the indirect method, operating net cash flow is calculated as follows: Begin with net income from the income statement. Add back noncash expenses, such as depreciation, amortization, and depletion.

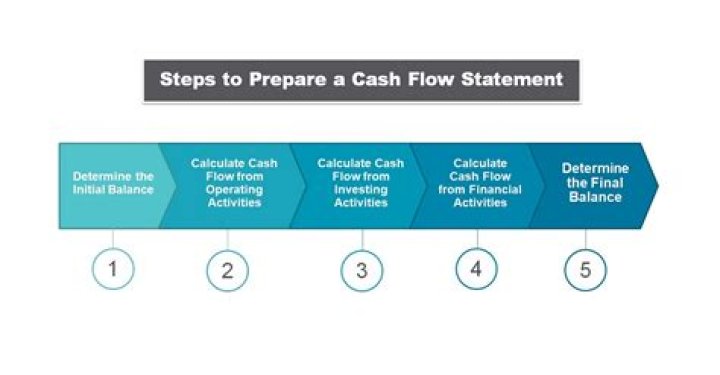

How to prepare Statement of cash flows by indirect method?

Preparing the operating section of statement of cash flows by the indirect method starts with net income from the income statement and adjusts for items that affect cash flows differently than they affect net income. Multiple levels of adjustments are required to reconcile accrual-based net income to cash flows from operating activities.

How does the operating section of the statement of cash flows work?

Starting indirectly with net income. When you use the indirect method of preparing the statement of cash flows, the operating section starts with net income from the income statement. You then adjust net income for any noncash items hitting the income statement.

How is net income adjusted in statement of cash flows?

The non-cash expenses and losses must be added back in and the gains must be subtracted. The next section of the operating activities adjusts net income for the changes in asset accounts that affected cash. These accounts typically include:

Which is an example of the direct method?

Using the direct method. The direct method of preparing the statement of cash flows shows the net cash from operating activities. This section shows all operating cash receipts and payments. Some examples of cash receipts you use for the direct method are cash collected from customers, as well as interest and dividends the company receives.