What are the various forms which are to be filled by individual and HUF while filing income tax return?

ITR-4 or Sugam The current ITR 4 applies to individuals and HUFs, Partnership firms (other than LLPs), which are residents and whose total income include: Business income according to the presumptive income scheme under section 44AD or 44AE. Professional income according to presumptive income scheme under section 44ADA.

Can HUF file ITR 1?

Who Can File ITR 1? -Resident Individuals & HUF can File this form. -Having Income from Salary or Pension, Other Income like Bank Interest, interest from IT Refund, Agricultural income up to Rs.

Can HUF file ITR 4?

ITR 4 is to be filed by the individuals/HUF/ Partnership firm whose total income of AY 2020-21 includes as below: Business income under section 44AD or 44AE. Income from Other Sources having income up to Rs 50 lakh (Excluding winning from lottery and income from horse races).

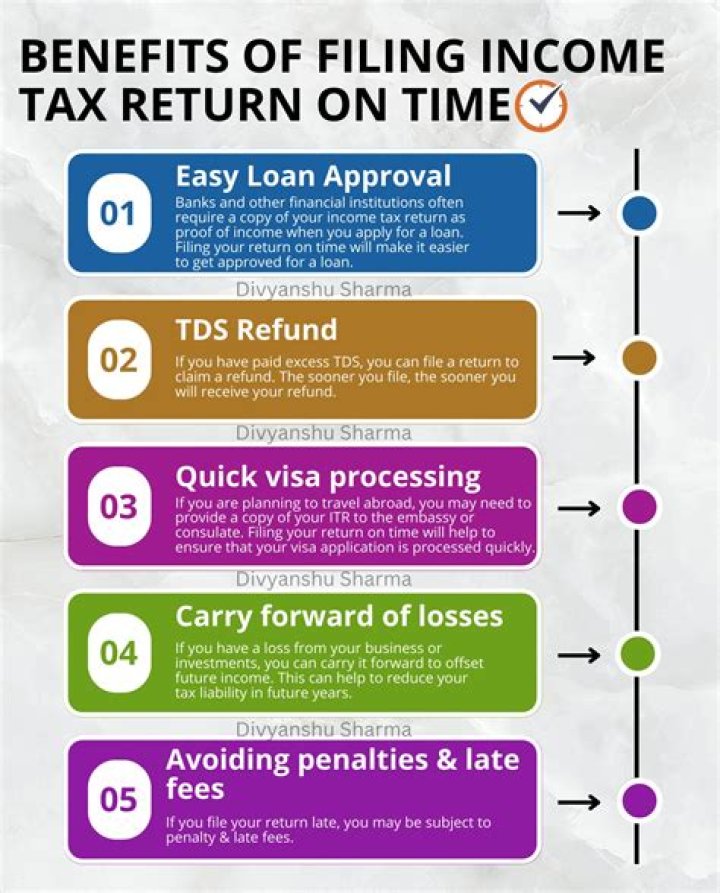

What are the types of returns?

3 types of return

- Interest. Investments like savings accounts, GICs and bonds pay interest.

- Dividends. Some stocks pay dividends, which give investors a share.

- Capital gains. As an investor, if you sell an investment like a stock, bond.

Is it compulsory to file ITR for HUF?

It is mandatory to file ITR if gross total income of an assessee, be it an individual, a Hindu Undivided Family (HUF), an Association of Persons (AOP) or a Body of Individuals (BOI), exceeds the maximum exemption limit. However, for a company or a firm, it is mandatory to file a return irrespective of income or loss.

Is it mandatory to file HUF return?

An Individual or HUF shall file his return of Income, even if income does not exceed the maximum exemption limit, if he has deposited an amount (or aggregate of amount) exceeding Rs. 1 crore in one or more current accounts maintained with a banking company or a co-operative bank. .

How is HUF treated in the Income Tax Act?

The HUF includes those persons who, by birth, acquire an interest in some joint family property. Under Section 2 (31) of the Income Tax Act, 1961 Hindu Undivided Family (HUF) is treated as a person and is taxed separately from its members.

How is a Hindu Undivided Family ( HUF ) taxed?

Under Section 2 (31) of the Income Tax Act, 1961 Hindu Undivided Family (HUF) is treated as a person and is taxed separately from its members. HUF includes all persons that are lineally descended from a common ancestor and will include their wives and their unmarried daughters. Two conditions must be satisfied to be assessed under the head of HUF:

Is the HUF a resident or non resident?

Excepting individual and HUF, all other persons are classified either as resident or non-resident. They are not to be further classified as ordinarily resident or as not ordinarily resident.

How to know residential status of individual, HUF, firm and Company?

To find out whether an individual is “ resident and ordinarily resident” in India, the following conditions have to be satisfied:- Basic conditions that need to be satisfied to check if an Individual is a resident in India are as follows:- 1) The person must be India in the previous year for a period of 182 days or more