What are UNICAP expenses?

Definition of UNICAP UNICAP stands for uniform capitalization, as noted above. In general, it refers to the set of tax rules governing how a business must account for its inventory. In other words, which normally-expensed costs must be capitalized for tax purposes and the manner in which those costs are determined.

How is 263A cost calculated?

263A costs allocable to eligible property remaining on hand at the close of the tax year under the MSPM is computed as follows: (Pre-production absorption ratio × Pre-production Sec. 471 costs remaining on hand at year end) + (Production absorption ratio × Production Sec. 471 costs remaining on hand at year end).

Who must do 263A?

Section 263a mainly applies to those who are either considered producers or resellers. Producers are those who build, install, manufacture, construct, or improve in or on property. Resellers are those who do not create inventory but rather purchase it and then resell it to another party.

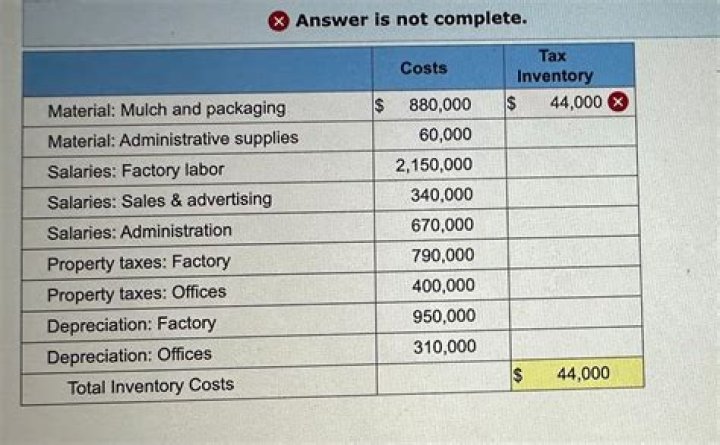

How is UNICAP calculated?

The first step is to calculate the absorption ratio – which is the additional 263A costs (those costs identified that are not already included in inventory for book purposes) divided by total inventory costs (Section 471 costs). This ratio is then multiplied by total ending inventory resulting in the UNICAP adjustment.

Who does Section 263A apply to?

What is service cost method?

The services cost method evaluates whether the amount charged for certain services is arm’s length by reference to the total services costs (as defined in paragraph (j) of this section) with no markup.

What are costs subject to capitalization under Section 263A?

Section 263A costs are defined as the costs that a taxpayer must capitalize under section 263A. Thus, section 263A costs are the sum of a taxpayer’s section 471 costs, its additional section 263A costs, and interest capitalizable under section 263A(f). (e)Types of costs subject to capitalization -. (1)In general.

When is a reseller not subject to Section 263A?

There are some instances where producers and resellers are not subject to Section 263a, but they are rather narrow. These instances include: For producers, if the cost of the property produced is de minimis , or less than 5% of the price that is charged to the customer.

What do you need to know about Section 263A?

Section 263a Overview. Section 263a is a section of the US tax code that contains the Uniform Capitalization, or UNICAP, rules, which describe how cost types and their amounts are to be capitalized, or expensed long term, instead of expensed in the current tax period. In this section, a taxpayer must account for each expense on their profit/loss…

How are additional SEC 263A costs calculated under MSPM?

In particular, the additional Sec. 263A costs allocable to eligible property remaining on hand at the close of the tax year under the MSPM is computed as follows: (Pre-productionabsorption ratio × Pre-productionSec. 471 costs remaining on hand at year end) + (Production absorption ratio × Production Sec. 471 costs remaining on hand at year end).