What causes contribution margin to increase?

Contribution Margin Increase The equation for contribution margin is the product’s revenue minus its variable costs, divided by the product’s revenue. If you reduce the variable costs of the product, you increase the product’s contribution margin.

Which of the following would cause an increase in the contribution margin ratio?

Contribution margin represents the difference between the selling price and the variable cost. Thus, the higher increase in selling price or lower decrease in the variable costs would result in an increase in contribution margin.

How do you increase contribution margin ratio?

How to Improve Contribution Margin

- Increase follow-on sales from existing customers.

- Raise the average invoice value of the initial and subsequent sales to a customer.

- Increase GM (Gross Margin) through price increases.

- Increase GM by reducing cost of goods sold (COGs)

Is lower contribution margin better?

The closer a contribution margin percent, or ratio, is to 100%, the better. The higher the ratio, the more money is available to cover the business’s overhead expenses, or fixed costs. If the contribution margin is extremely low, there is likely not enough profit available to make it worth keeping.

How do you find the contribution margin ratio?

How to Calculate Contribution Margin

- Net Sales – Variable Costs = Contribution Margin.

- (Product Revenue – Product Variable Costs) / Units Sold = Contribution Margin Per Unit.

- Contribution Margin Per Unit / Sales Price Per Unit = Contribution Margin Ratio.

What is the formula for the contribution margin ratio?

Net Sales – Variable Costs = Contribution Margin The two primary variables here are net sales and variable costs, both of which can be found on an income statement.

What affects the contribution margin?

The contribution margin per unit inherently goes down if a company has the same variable costs but lowers the price per unit for a certain product. Ironically, it may achieve a higher total contribution margin if a subsequent increase in volume outweighs the lower contribution margin per unit.

What does contribution margin indicate?

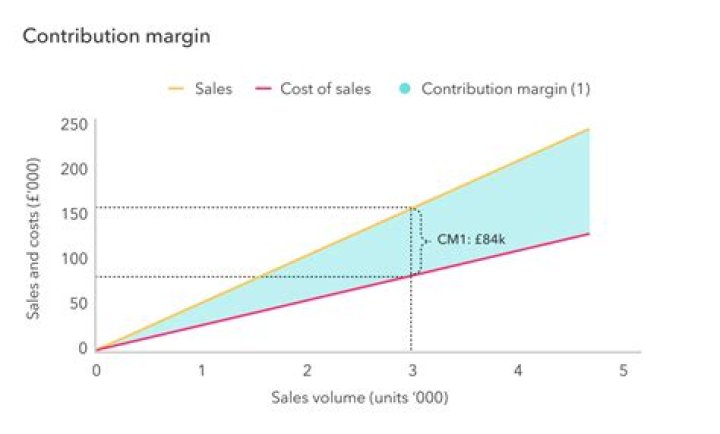

The contribution margin represents the portion of a product’s sales revenue that isn’t used up by variable costs, and so contributes to covering the company’s fixed costs. The concept of contribution margin is one of the fundamental keys in break-even analysis.

What does contribution margin tell you?

“Contribution margin shows you the aggregate amount of revenue available after variable costs to cover fixed expenses and provide profit to the company,” Knight says. You might think of this as the portion of sales that helps to offset fixed costs.

Which of the following is the way to calculate contribution margin ratio?

The contribution margin ratio can be calculated by subtracting the variable cost ratio from one. Variable expense per unit consists only of direct materials, direct labor, and variable overhead. The break-even point in sales dollars is equal to the break-even units multiplied by cost.

What is difference between contribution margin and gross margin?

Gross margin is the amount of money left after subtracting direct costs, while contribution margin measures the profitability of individual products. Contribution margin can be used to examine variable production costs and is usually expressed as a percentage.

What is the result when the contribution margin ratio increases?

Contribution Margin Increase The contribution margin ratio increases when sales increase. For every $1 increase in sales, profits increase by the contribution margin ratio. For example, if a company’s contribution margin ratio is 25 percent, it is earning roughly 25 cents in profit for every one dollar in sales.

Does contribution margin increase when sales increase?

Increases sales at the same margin lead to a higher total contribution margin.

What factors affect contribution margin?

Contribution margin is usually higher than gross margin because it doesn’t include all costs of goods sold.

- Materials or Product Costs. The cost of materials or product acquisitions are among the key variable product costs considered in the contribution margin.

- Variable Expenses.

- Improved Efficiencies.

- Price Changes.

When does contribution margin ratio begin to decrease?

D. the contribution margin ratio begins to decrease. The contribution margin ratio always increases when the? A. variable expenses as a percentage of sales increase. B. variable expenses as a percentage of sales decrease.

How are fixed and variable costs related to contribution margin?

Fixed costs are production costs that remain the same as production efforts increase. Variable costs, on the other hand, increase with production levels. The contribution margin measures how efficiently a company can produce products and maintain low levels of variable costs.

What is the contribution margin of sales revenue?

The result of this calculation shows the part of sales revenue that is not consumed by variable costs and is available to satisfy fixed costs, also known as the contribution margin .

What is a good contribution margin percentage?

Most likely, however, the contribution margin will come in at much less than 100 percent, and maybe even less than 50 percent. In reality, a “good” contribution margin is all relative, depending on the nature of a given company, its expense structure, and whether the company is competitive with its business peers.