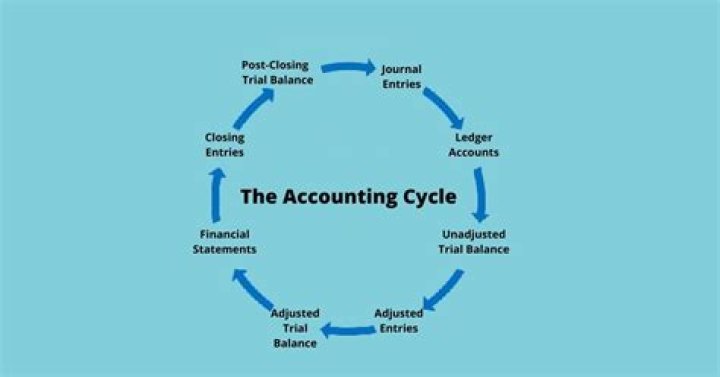

What do you mean by accounting principles?

Accounting principles are the rules and guidelines that companies must follow when reporting financial data. The Financial Accounting Standards Board (FASB) issues a standardized set of accounting principles in the U.S. referred to as generally accepted accounting principles (GAAP).

What are the accounting principles and concepts?

There are four main conventions in practice in accounting: conservatism; consistency; full disclosure; and materiality.

What is the three golden rules of accounting?

Take a look at the three main rules of accounting: Debit the receiver and credit the giver. Debit what comes in and credit what goes out. Debit expenses and losses, credit income and gains.

What are the four fundamentals of accounting?

There are four basic principles of financial accounting measurement: (1) objectivity, (2) matching, (3) revenue recognition, and (4) consistency.

What is accounting principles and concepts?

Accounting Concepts and Principles are a set of broad conventions that have been devised to provide a basic framework for financial reporting. Accountants must therefore actively consider whether the accounting treatments adopted are consistent with the accounting concepts and principles.

What do you mean by generally accepted accounting principles?

How to define accounting principles in SAP menu path?

IMG –> Financial Accounting –> Financial Accounting Global Settings –> Company Code –> Parallel Accounting –> Accounting Principles and additional Ledgers –> Define Accounting Principles

How to define accounting principles in SAP IMG?

SAP IMG –> Financial Accounting (New) –> General Ledger accounting (New)–> Financial Accounting Global Settings (New) –> Ledgers –> Parallel Accounting –> Define Accounting Principle. Step 1) Follow the menu path and double click on “Define accounting principles”.

What are the principles of accounting under GAAP?

There are some of the main accounting principles and guidelines, listed under US GAAP: Conservatism principle – In situations where there are two acceptable solutions for reporting an item, the accountant should ‘play it safe’ by choose the less favourable outcome.