What does 1031 exchange stand for in real estate?

Updated Mar 12, 2021 In real estate, a 1031 exchange is a swap of one investment property for another that allows capital gains taxes to be deferred. The term, which gets its name from IRS code…

What does section 1031 of the Internal Revenue Code mean?

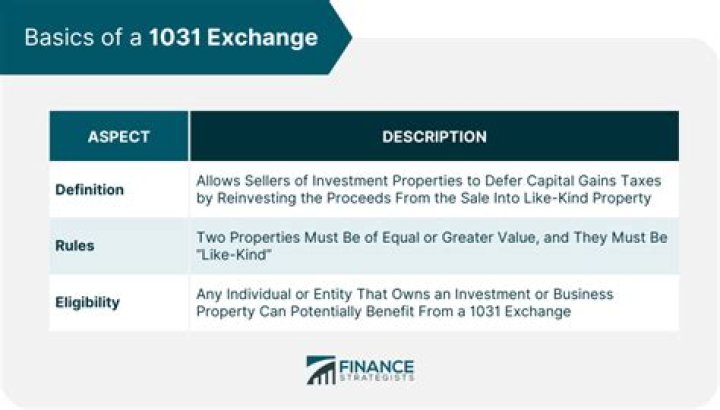

Section 1031 of the Internal Revenue Code allows a taxpayer to defer the recognition of gains (or losses) on an investment property when sold if the relinquished property is exchanged for a like-kind replacement property.

Can a 1031 exchange apply to a former primary residence?

The 1031 provision is for investment and business property, although the rules can apply to a former primary residence under certain conditions.

What happens to depreciable property in a 1031 exchange?

Warning: Special rules apply when depreciable property is exchanged in a 1031. It can trigger a gain known as “depreciation recapture” that is taxed as ordinary income. In general, if you swap one building for another building you can avoid this recapture.

How long does it take to replace a property in a 1031 exchange?

From the time of closing on the relinquished property, the investor has 45 days to nominate potential replacement properties and a total of 180 days from closing to acquire the replacement property. Identification requirements: The investor must identify the replacement property prior to midnight on the 45th day.

Who is required to sign 1031 exchange closing instructions?

The buyer also signs this agreement to acknowledge the 1031 exchange transaction. This is the only document the Buyer is required to sign. Exchange Closing Instructions. The Exchange Closing Instructions should be signed by you as the escrow officer, closing or settlement agent prior to closing.

What are the closing instructions for Exeter 1031 exchange?

Acceptable language would be: Exeter 1031 Exchange Services, LLC and the client must sign and approve any and all escrow instructions, preliminary title reports or commitments and estimated closing statements.

When was section 1031 added to the Internal Revenue Code?

Section 1031 has existed in the Internal Revenue Code since the first Code in 1939. It remains identical with only two additions in more than 75 years. Section 1031 on its face appears to permit only a direct exchange of properties between two taxpayers.

Can a related party exchange be disallowed under Section 1031?

Related party transactions are an enigma under many provisions of the Internal Revenue Code. Section 1031 (f) provides that if a Taxpayer exchanges with a related party then the party who acquired the property in the exchange must hold it for 2 years or the exchange will be disallowed.

What kind of property does section 1031 not apply to?

Keep in mind that Section 1031 does not apply to exchanges of inventory, stocks, bonds, notes, evidence of indebtedness, and certain other assets. Beginning in 2018, new tax legislation limited these exchanges to real estate: Section 1031 exchanges of other property, such as artwork, are no longer permitted.

Where do I report a 1031 exchange on my tax return?

All 1031 exchanges are reported on IRS Form 8824. This is where you describe the relinquished and replacement property, the dates the relinquished property was acquired and transferred, the dates the replacement property was identified and received, and information about related parties.

Do you get cash proceeds from 1031 exchange?

By its very nature, a 1031 exchange means you aren’t entitled to any cash proceeds from relinquishing your asset. Finally, deferring tax payments through an asset exchange isn’t always a sound business plan.

What are the limitations of the 1031 exchange agreement?

The 1031 Exchange Agreement must also specifically limit the investor’s rights to receive, pledge, borrow or otherwise obtain the benefits of the relinquished property sale proceeds prior to the expiration of the exchange period. This restriction on use of funds is comprehensive and is often called the ” (g) (6) limitations.”

When to exchange real property held for sale?

This subsection shall not apply to any exchange of real property held primarily for sale. such property is not identified as property to be received in the exchange on or before the day which is 45 days after the date on which the taxpayer transfers the property relinquished in the exchange, or

Is there a capital gain exclusion on a 1031 exchange?

The 1031 delayed any recognition of gain. Later they moved into the new property, made it their primary residence and eventually planned to use the $500,000 capital gain exclusion. In 2004 Congress tightened that loophole. Yes, taxpayers can still turn vacation homes into rental properties and do 1031 exchanges.

Is there a limit to how often you can do a 1031 exchange?

If used correctly, there is no limit on how many times or how frequently you can do 1031 exchanges. The rules can apply to a former primary residence under very specific conditions.

What is the 1031 exchange for Dummies called?

One of the least known but fastest growing types of exchange is the construction exchange. Also called the improvement or build-to-suit exchange, it allows you to make improvements to your replacement property during the 180-day window. The 1031 exchange is for dummies, and for savvy investors too.

How long does it take for a 1031 exchange to be completed?

●1031 exchanges carried out within 180 days are commonly referred to as delayed exchanges, since, at one time, exchanges had to be performed simultaneously. ● Build-to-suit exchanges allow the replacement property in a 1031 exchange to be renovated or newly constructed.

What happens if the 1031 exchange is cut?

The loss of the 1031 exchange would greatly reduce incentives for developers to build more units due to loss of profitability and reduce real estate capital investment and development, which would be truly detrimental to communities at a time when the U.S. is desperately in need of economic expansion.

Can a partnership be used in a 1031 exchange?

Interest in a partnership cannot be used in a 1031 exchange—partners in an LLC do not own property, they own interest in a property-owning entity, which is the taxpayer for the property. 1031 exchanges are carried out by a single taxpayer as one side of the transaction.