What does life annuity protect against?

In essence, you can create your own “pension plan” by choosing an immediate annuity with a lifetime payout option. This protects you from longevity risk—the chance that you may live longer than your financial resources can support you.

How are annuities protected?

Annuities are regulated and protected at the state level. Every state has a nonprofit guaranty organization that each insurance company operating in that state must join. In the event that a member company fails, the other companies in the guaranty association help pay the outstanding claims.

Are annuities protected by FDIC?

The FDIC does not insure money invested in stocks, bonds, mutual funds, life insurance policies, annuities or municipal securities, even if these investments are purchased at an insured bank.

How are fixed annuities protected in the US?

While this is true, consumers can be confident their fixed annuities ARE strongly protected. In fact each annuity already comes insured by the company who issued the annuity. And, if the insurance company fails, it has secondary protection from the state guaranty association up to a maximum amount, as with the FDIC, determined by each state.

Why are annuities important in a diversified retirement portfolio?

Annuities can be an important part of a diversified retirement portfolio because they can ensure that your retirement income is protected even when there are downturns in the market.

How does a deferred annuity fund work?

Deferred annuities begin paying out at a later date and include an accumulation period during which the account value grows as interest is compounded. The annuity fund for a fixed annuity comprises bonds and other fixed-rate investments into which the insurance company invests the money.

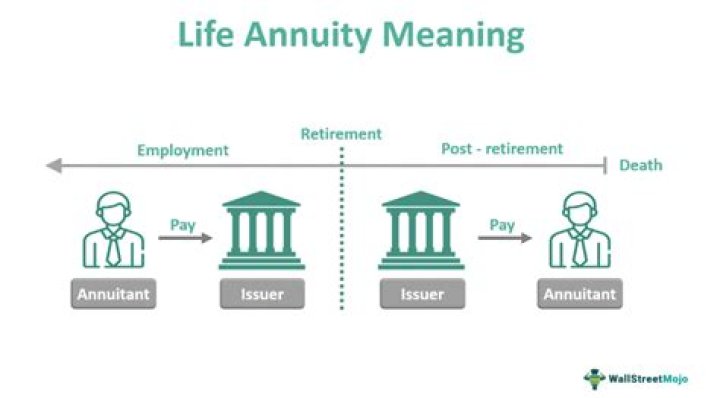

What’s the difference between an annuity and a pension?

Annuities insure retirees against the risks of outliving their retirement savings (longevity risk) or losing savings due to low or negative investment returns (investment risk). In general, an annuity pays a monthly amount for the remainder of the annuitant’s life in exchange for a one-time upfront payment called a premium.