What does positive deferred income tax mean?

A deferred income tax is a liability recorded on a balance sheet resulting from a difference in income recognition between tax laws and the company’s accounting methods. For this reason, the company’s payable income tax may not equate to the total tax expense reported.

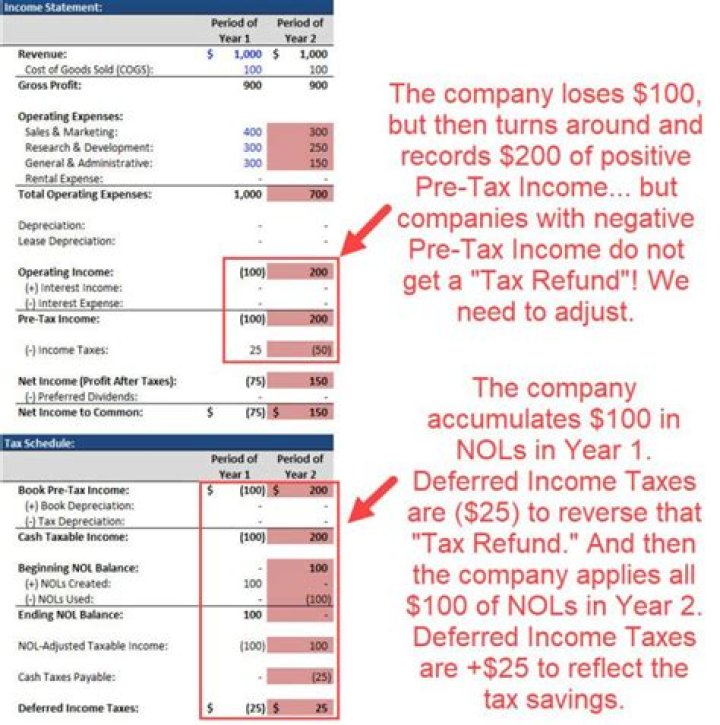

Why would Deferred income tax increase?

Reason for Increase If the company experiences continued losses from operations or from balance sheet adjustments, the amount shown as a deferred tax asset will increase by the amount of these losses and adjustments.

Can Deferred income tax be negative?

Deferred tax assets. If the temporary difference is positive, a deferred tax liability will arise. If the temporary difference is negative, a deferred tax asset will arise.

What is provision from income tax?

A provision for income taxes is the estimated amount that a business or individual taxpayer expects to pay in income taxes for the current year. The adjusted net income figure is then multiplied by the applicable income tax rate to arrive at the provision for income taxes.

Why is there a provision for deferred tax?

The reason for recording deferred taxes is to provide for increase or decrease in the tax liability due to timing differences that arise owing to various disallowances under Income Tax act. Some of the timing differences examples are Depreciation u/s 32, deductions based on actual payment u/s 43B,etc.

Why is deferred tax liability higher than taxable income?

Since the straight-line method produces lower depreciation when compared to that of the under accelerated method, a company’s accounting income is temporarily higher than its taxable income. The company recognizes the deferred tax liability on the differential between its accounting earnings before taxes and taxable income.

What are the permanent differences in deferred tax?

Permanent differences are the differences between taxable income and accounting income for a period that originate in one period and do not reverse subsequently.” Deferred tax is brought into accounts to make the clear picture of current tax and future tax.

How to calculate deferred tax as per income statement?

Calculation of Deferred Tax Particulars As per Income Statement (Rs.) As per Tax Statement (Rs.) Total income 1800000 1800000 Expenses 1200000 1200000 Gross profit before depreciation and tax 600000 600000 Depreciation 120000 100000