What does the term structure of interest rates indicate?

The term structure of interest rates reflects the expectations of market participants about future changes in interest rates and their assessment of monetary policy conditions. In general terms, yields increase in line with maturity, giving rise to an upward-sloping, or normal, yield curve.

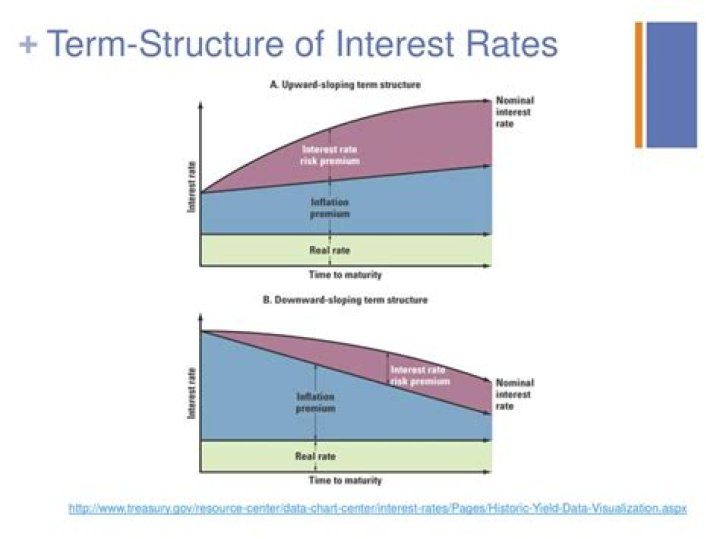

What is the term structure of interest rates and how is it related to the yield curve?

The term structure of interest rates is upward sloping when long-term rates are higher than short-term rates. An upward sloping yield curve is called a normal yield. When short-term rates are higher than the long-term rates, then term structure is downward sloping.

How do the risk and term structure affect interest rates?

Chapter 5 How Do Risk and Term Structure Affect Interest Rates? How Do Risk and Term Structure Affect Interest Rates? The bond with a C rating should have a higher risk premium because it has a higher default risk, which reduces its demand and raises its interest rate relative to that on the Baa bond.

What are the theories of term structure?

The theories that attempt to explain the term structure of interest rates are: the expectations theory, market segmentation theory, and liquidity preference theory. The term structure is not easily observed in the market and as a result spot and forward are derived from the coupon curve.

What are term rates?

: the reduced rate that applies to a term policy.

What is forward interest rate?

A forward rate is an interest rate applicable to a financial transaction that will take place in the future. The term may also refer to the rate fixed for a future financial obligation, such as the interest rate on a loan payment.

What is considered a normal yield curve?

The normal yield curve is a yield curve in which short-term debt instruments have a lower yield than long-term debt instruments of the same credit quality. This gives the yield curve an upward slope. This is the most often seen yield curve shape, and it’s sometimes referred to as the “positive yield curve.”

What is the default risk premium?

A default risk premium is effectively the difference between a debt instrument’s interest rate and the risk-free rate. The default risk premium exists to compensate investors for an entity’s likelihood of defaulting on their debt.

What is the term structure of interest rates quizlet?

The term structure of interest rates is the relationship between interest rates or bond yields and different terms or maturities. The term structure of interest rates is also known as a yield curve, and it plays a central role in an economy.

What is current spot rate?

The spot rate is the current price quoted for immediate settlement of the contract. For example, if during the month of August a wholesale company wants immediate delivery of orange juice, it will pay the spot price to the seller and have orange juice delivered within two days.

How do you calculate forward rate?

A three-month forward rate is equal to the spot rate multiplied by (1 + the domestic rate times 90/360 / 1 + foreign rate times 90/360). To calculate the forward rate, multiply the spot rate by the ratio of interest rates and adjust for the time until expiration.

What is a zero rate?

A bond with a coupon rate of zero, therefore, is one that pays no interest. This means that, as interest rates go up or down, the market value of bonds fluctuates depending on if their coupon rates are higher or lower than the current interest rate.

What is the current shape of the yield curve?

The current yield curve shows all U.S.-issued securities and their rates of return. An upward curve suggests that investors expect healthy economic growth. A downward curve is seen as a warning of a recession ahead.

What is a healthy yield curve?

The normal yield curve is a yield curve in which short-term debt instruments have a lower yield than long-term debt instruments of the same credit quality. This gives the yield curve an upward slope. Analysts look to the slope of the yield curve for clues about how future short-term interest rates will trend.

How do I calculate default risk premium?

The default risk premium is essentially the anticipated return on a bond minus the return a similar risk-free investment would offer. To calculate a bond’s default risk premium, subtract the rate of return for a risk-free bond from the rate of return of the corporate bond you wish to purchase.

What is default risk premium and give it an example?

Default risk premium: The component of the interest rate that compensates investors for the higher credit risk from the issuing company. A default occurs when a company misses an interest payment to its bondholders, so a default risk premium is intended to offset this risk with higher interest payments.

What is rate and term option ratio?

A “rate-and-term” refinance: Borrowers simply adjust the interest rate and term of their mortgage while maintaining the original remaining principal amount. Instead of shrinking or enlarging the mortgage balance, this option leaves it unchanged.