What does the vertical analysis tell you?

Vertical analysis makes it easier to understand the correlation between single items on a balance sheet and the bottom line, expressed in a percentage. Vertical analysis can become a more potent tool when used in conjunction with horizontal analysis, which considers the finances of a certain period of time.

What is a vertical and horizontal analysis?

Vertical analysis is also known as common size financial statement analysis. For example, the vertical analysis of an income statement results in every income statement amount being restated as a percent of net sales. Horizontal analysis is also referred to as trend analysis.

What is vertical common size analysis?

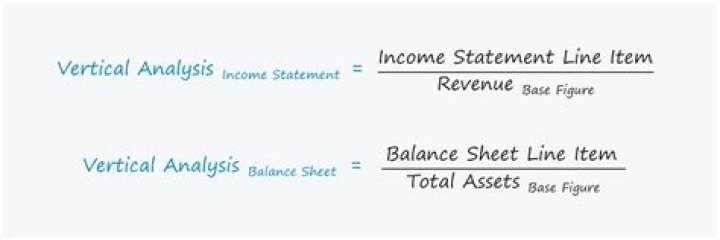

Common size analysis, also referred as vertical analysis, is a tool that financial managers use to analyze financial statements. In the balance sheet, the common base item to which other line items are expressed is total assets, while in the income statement, it is total revenues.

What are the objectives of trend analysis?

The purpose of trend analysis is to spot a prevalent trend within a user group and/or to determine how a trend developed/would develop over time. This exercise helps identify new opportunities and ideas for concepts or products.

What is the difference between vertical and financial analysis?

In Horizontal Financial Analysis, the comparison is made between an item of financial statement, with that of the base year’s corresponding item. On the other hand, in vertical financial analysis, an item of the financial statement is compared with the common item of the same accounting period.

Which analysis is considered as static?

Static code analysis is a method of debugging by examining source code before a program is run. It’s done by analyzing a set of code against a set (or multiple sets) of coding rules. Static code analysis and static analysis are often used interchangeably, along with source code analysis.

Which are the types of financial analysis?

Types of financial analysis

- Horizontal Analysis. This involves the side-by-side comparison of the financial results of an organization for a number of consecutive reporting periods.

- Vertical Analysis.

- Short Term Analysis.

- Multi-Company Comparison.

- Industry Comparison.

- Valuation Analysis.

- Related Courses.