What does waiving rights to a joint and survivor annuity?

When the participant dies, the spouse will receive lifetime payments in the same or reduced amount. The participant may waive the Qualified Joint and Survivor Annuity with spousal consent and elect to receive another form of payment.

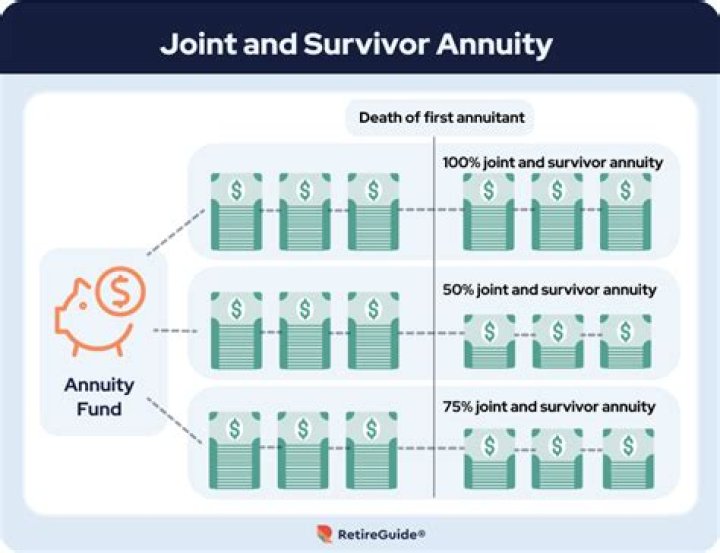

How do joint and survivor annuities work?

What Is a Joint and Survivor Annuity? A joint and survivor annuity is an annuity that pays out for the remainder of two people’s lives. A 50 percent joint and survivor annuity will pay the surviving annuitant half the payment amount that payees were receiving when both annuitants were alive.

Can an annuity be held in a joint account?

An annuity owner can also set up the account with joint annuitants such as in the case of husband and wife. In this situation, the disbursement would be different than a single annuitant. Even if there are two annuitants, one must take ownership of the annuity so as to establish and maintain the account.

What is a joint and survivor annuity?

A joint and survivor annuity is an insurance product for couples that continues to make regular payments as long as one spouse lives. There are also provisions for making payments to a third party when both annuitants die before monthly payments have exceeded the principal.

What is a joint or survivor annuity?

Can a surviving spouse be the joint owner of an annuity?

But that rule triggers based on whether the spouse is named as the beneficiary, not the joint owner. In fact, once a surviving spouse is properly named as a beneficiary, there’s often no reason at all for the annuity to be jointly owned anymore!

What happens to a spousal annuity if you retire?

If you marry after you retire, you can elect a spousal annuity. If you do, there will be two reductions in your annuity. One is the standard reduction to provide the survivor annuity. This reduction would be eliminated if your marriage were to end. The second is a permanent actuarial reduction to pay the survivor annuity deposit.

What are the disadvantages of a joint and Survivor Annuity?

In addition to the lower payments, joint and survivor annuities restrict the surviving spouse’s ability to access a large sum of cash because, in contrast to the variety of payout options available to beneficiaries of single-life annuities, the only option with a joint and survivor annuity is to continue with the existing payment schedule.

Do you have to be a spousal beneficiary for a non qualified annuity?

Notably, though, a key distinction of the spousal continuation provision for a non-qualified annuity is that the driving factor to allow continued tax deferral is not the joint ownership of the annuity, but the spousal beneficiary of the contract.